There is a strand of economic thought that has always sat at an uncomfortable angle to the mainstream. It does not chase mathematical elegance the way neoclassical economics does. It is suspicious of macroeconomic aggregates and the policy interventions built on top of them. It insists that the individual human being, acting purposefully and valuing things subjectively, must remain the starting point for any honest economic analysis. This is the Austrian School of Economics, and its ideas have done more to shape the intellectual foundation of libertarianism than any other academic tradition.

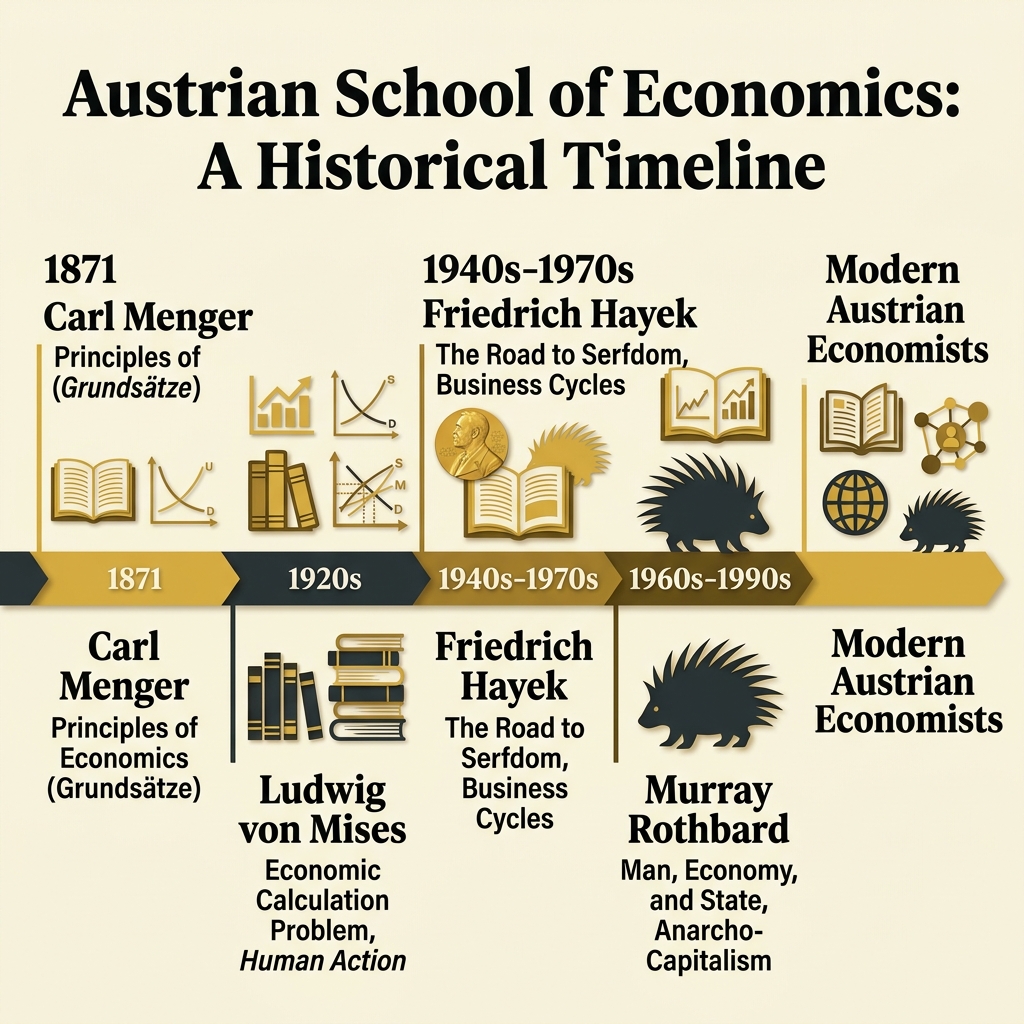

The Austrian School began in Vienna in 1871, came of age in the salons and seminars of interwar Europe, survived exile and dismissal, and eventually experienced a remarkable revival in the second half of the twentieth century. Its central insights about prices, markets, knowledge, and the distortions caused by government intervention remain as relevant today as they were when Carl Menger first put them on paper.

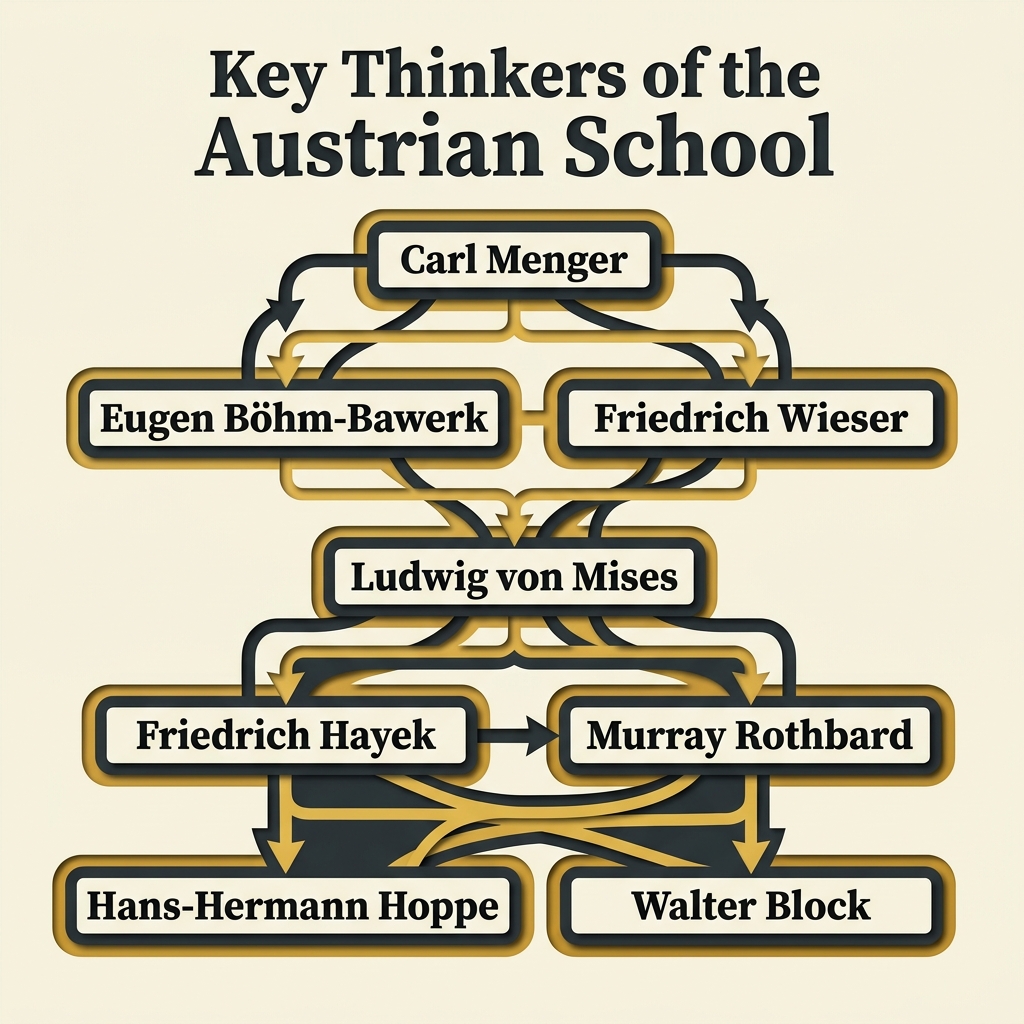

The Founding: Carl Menger and the Subjective Revolution

Before 1871, economists were stuck on a puzzle they called the paradox of value. Water, which is essential to human life, is nearly free. Diamonds, which are not essential to anything, cost a fortune. The labor theory of value, which dominated classical economics through Adam Smith and David Ricardo and later became the backbone of Marx's political economy, could not explain this. If value comes from the labor needed to produce something, why does water cost so little and a diamond so much?

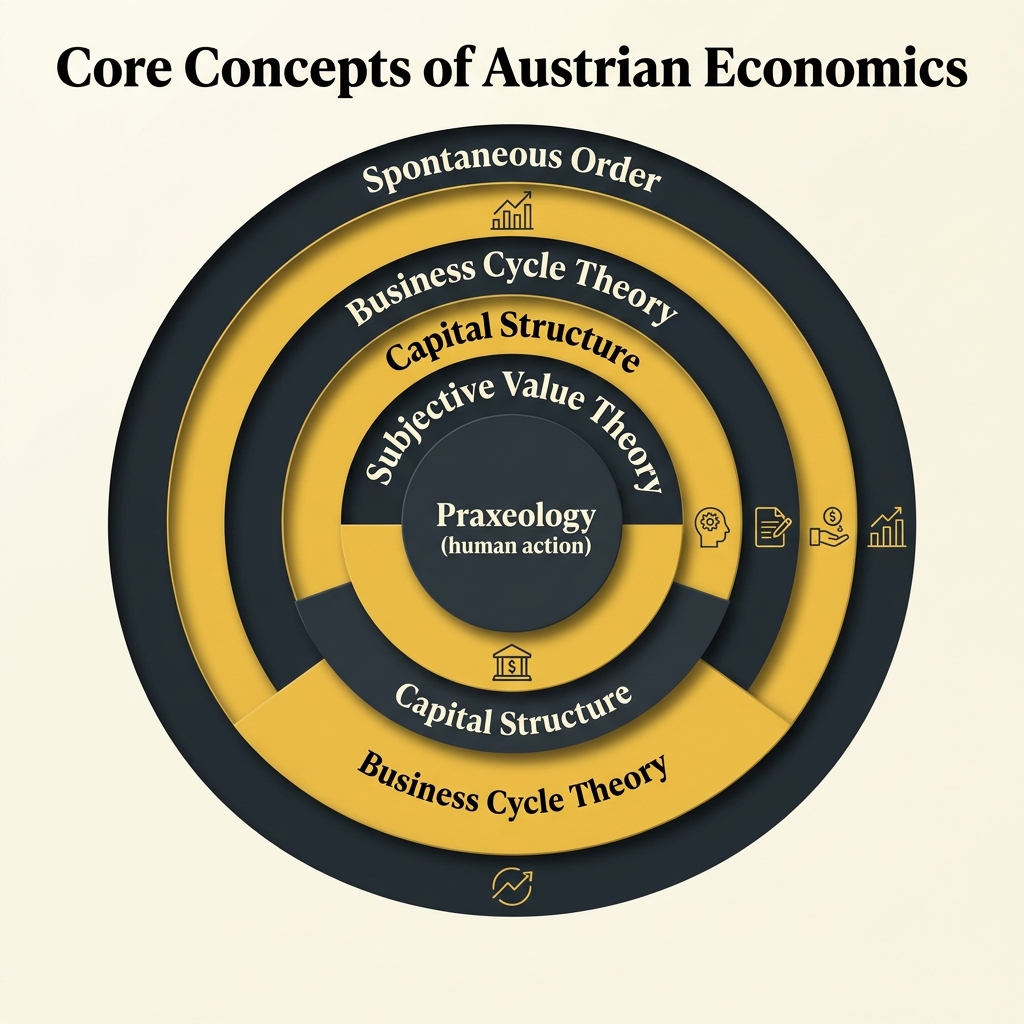

Carl Menger, a Viennese economist, solved this problem in his 1871 Principles of Economics (Grundsatze der Volkswirtschaftslehre). His solution was both simple and profound: value is not inherent in goods. It is conferred on them by the choices of human beings in specific circumstances. A person dying of thirst values the first cup of water enormously. The hundredth cup means very little. This is diminishing marginal utility, and it explains the diamond-water paradox immediately. At the margin, where actual decisions are made, water is abundant and diamonds are scarce.

This insight is called the subjective theory of value, and it changed everything. If value is subjective, then prices cannot be set by government planners or labor inputs. Prices are signals that emerge from the choices of millions of individuals, each acting on their own preferences and knowledge. No authority can know in advance what those choices will be, which means no authority can determine in advance what the "correct" price of anything should be.

At almost exactly the same moment, William Stanley Jevons in England and Leon Walras in Switzerland independently arrived at similar conclusions about marginal utility. This simultaneous discovery is known as the Marginal Revolution. But Menger's version differed from those of Jevons and Walras in important ways. Menger was skeptical of mathematical formalism in economics and more interested in the causal genetic process by which economic phenomena come about. These differences in method would shape the distinct character of the Austrian School for the next century.

The First Generation: Bohm-Bawerk, Wieser, and Capital Theory

Menger's students carried his insights forward in powerful directions. Eugen von Bohm-Bawerk (1851-1914) developed a comprehensive theory of capital and interest that remains influential today. His central argument was that production takes time, and time has a value. Roundabout methods of production, those that involve more stages and more time, tend to be more productive than direct methods. A fisherman who takes time to weave a net catches more fish in the long run than one who simply wades in and grabs fish by hand.

The rate of interest, in Bohm-Bawerk's framework, is the price of time preference: the premium that people demand for deferring consumption now in exchange for more consumption later. This insight has profound implications for monetary policy. If the interest rate is artificially suppressed below its natural market level, it sends a false signal. Businesses see cheap credit and invest in longer-term, more roundabout production processes, as if consumers had decided to save more and were willing to defer consumption. But the consumers have not actually changed their preferences. The signal was a lie. When the truth emerges, the malinvestments unravel.

Friedrich von Wieser (1851-1926) contributed the concept of opportunity cost, the idea that the true cost of any choice is the value of the best alternative foregone. This is now standard in economics textbooks, but Wieser's formulation was tied to a broader insight: resources always have alternative uses, and the value assigned to a resource in one use reflects what it could produce elsewhere. Wieser also elaborated on the concept of imputation, the process by which the value of final consumer goods is attributed back to the factors of production that created them.

Ludwig von Mises: The System Builder

Ludwig von Mises (1881-1973) was the most systematic and ambitious thinker the Austrian School produced. He entered the intellectual scene at a critical moment: the late nineteenth and early twentieth centuries were a period of intense debate over socialism. Could socialist planning work? Could a government agency successfully manage a modern industrial economy?

In 1920, Mises published an article, later expanded into the book Socialism (1922), that many regard as one of the most important contributions to economic and political thought in the twentieth century. His argument was that socialist central planning was not merely inefficient but logically impossible. The reason: economic calculation requires prices, and prices require a market, and a market requires private property. Without private ownership of the means of production, there can be no genuine market for those means. Without such a market, there are no prices. Without prices, planners have no way to allocate resources rationally. They cannot know whether to build a steel mill or a coal mine first, whether to route resources into consumer goods or capital goods, whether a particular production process is economical or wasteful. They would be, as Mises put it, groping in the dark.

"The human mind cannot orient itself properly among the bewildering mass of intermediate products and potentialities of production without such aid. It would simply stand perplexed before the problems of management and location."

Ludwig von Mises, Socialism (1922)

This argument, known as the socialist calculation problem, sparked a decades-long debate. Oskar Lange and Abba Lerner argued that socialist planners could simulate market prices. Mises and Hayek rejected this: simulated prices are not real prices, because they are not generated by actual ownership and actual exchange. Without the feedback mechanism of profit and loss, there is no way for planners to know whether their calculations are right or wrong. The collapse of Soviet-style economies in the late twentieth century did not conclusively prove Mises right, but it did validate his skepticism in a very visible way.

Mises's masterwork was Human Action (1949), a comprehensive treatise on economics built from the ground up on what he called praxeology: the logic of human action. Every human action, Mises argued, involves a purposeful being choosing among alternatives to achieve a goal. From this simple starting point, he derived an enormous superstructure of economic theory: the nature of value and exchange, the function of money and prices, the theory of capital and interest, the business cycle, and the inevitable failure of government intervention. The book is long and demanding, but it is the most thorough statement of the Austrian economic worldview ever written.

Friedrich Hayek: Knowledge, Prices, and the Road to Serfdom

Friedrich Hayek (1899-1992) extended and deepened the Austrian tradition in two major directions. The first was his development of the knowledge problem, which he stated most precisely in his 1945 paper "The Use of Knowledge in Society." The second was his application of Austrian ideas to the political question of whether central planning was compatible with a free society.

The knowledge problem is simple to state and far-reaching in its implications. The information relevant to economic coordination, Hayek argued, is not concentrated in any one place. It is dispersed among millions of individuals: the farmer who knows the soil conditions of his particular field, the businessman who knows the particular tastes of his local customers, the worker who knows the particular capabilities of the machine she operates every day. This knowledge is local, tacit, and constantly changing. It cannot be aggregated and transmitted to a central planner, because much of it exists only as practical know-how, not as something that can be written down and sent to a central office.

The price system solves this problem through a remarkable process. When the supply of copper falls in one corner of the world, copper prices rise everywhere. Manufacturers in countries that had never heard of the original disruption begin economizing on copper, switching to substitutes, and finding new sources. They do not need to know why copper prices rose. They only need to know that it did rise. The price system compresses and transmits the relevant information in a form that guides action without requiring anyone to understand the whole picture. No central planner, however intelligent, could replicate this function.

In The Road to Serfdom (1944), written during World War II and addressed to the British left, Hayek made a more explicitly political argument. Central economic planning, he argued, is not compatible with political freedom. The reason is that planning requires a plan, and a plan requires an agreement on ends. A free society is precisely one in which people with different ends, different values, and different visions of the good life can coexist without having to impose their values on each other. The moment a government begins centrally directing economic life, it must decide whose ends matter, which values deserve resources, which ways of life are worth supporting. These decisions cannot be made democratically: they require a degree of authority and coercion that is fundamentally incompatible with the freedom that democracy is supposed to protect.

Hayek won the Nobel Prize in Economics in 1974, shared with Gunnar Myrdal, a Keynesian. The Nobel committee's decision was widely seen as a deliberate pairing of opposites. Hayek used his Nobel lecture, "The Pretense of Knowledge," to argue that the failure of Keynesian economic management in the stagflation of the early 1970s was not an accident but a consequence of economists overestimating their ability to manage what they did not fully understand.

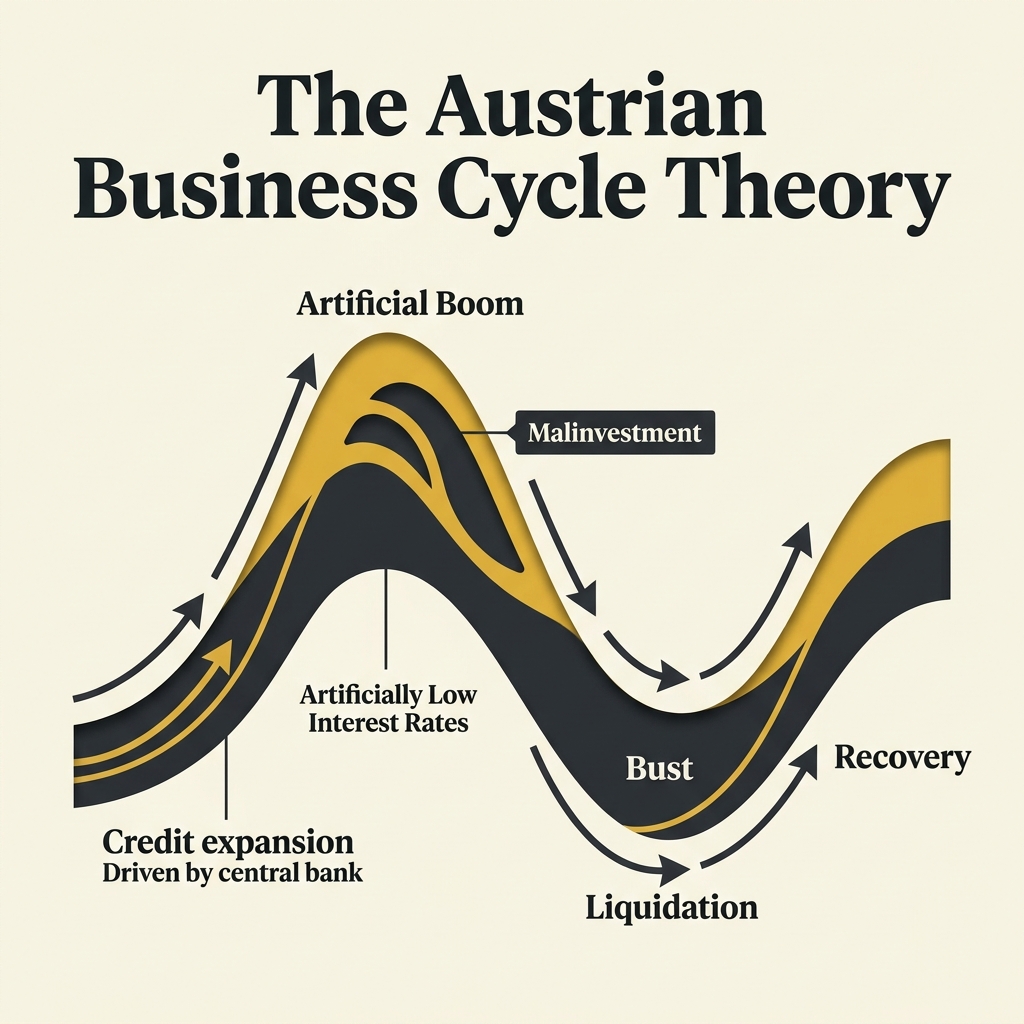

The Austrian Business Cycle Theory

One of the most distinctive and controversial contributions of the Austrian School is its theory of the business cycle. Developed by Mises and extended by Hayek, the Austrian Business Cycle Theory (ABCT) explains booms and busts not as random fluctuations or failures of aggregate demand, but as the predictable consequences of credit expansion by central banks.

The argument runs as follows. When a central bank artificially lowers interest rates below their natural market level (the level that would balance the supply of savings with the demand for investment), businesses receive a false signal. Low interest rates normally indicate that consumers are saving more, deferring current consumption in favor of future consumption, and therefore that resources are available for long-term investment. Businesses respond by starting more capital- intensive, time-consuming projects: new factories, infrastructure, technology development.

But if the low interest rates are artificial, the signal is wrong. Consumers have not actually decided to save more. They are still spending at the old rate. The economy has simultaneously expanded its investment and maintained its consumption, which is not sustainable. The additional investment has been funded not by real savings but by newly created credit. The structure of production has become distorted: too many resources are tied up in long-term projects that consumers will not actually want to buy when the projects are complete.

At some point, the unsustainable nature of the boom becomes apparent. Interest rates begin to rise as the credit expansion slows. Businesses that had started long-term projects find they cannot complete them profitably. Malinvestments are revealed: the factories, buildings, and production lines that were started during the boom but have no viable economic future are abandoned or sold at a loss. The bust is not a random shock. It is the economy's way of correcting the distortions created by the boom.

From this perspective, the appropriate response to a recession is not to stimulate aggregate demand, as Keynesians argue, but to allow the liquidation of malinvestments to proceed as quickly as possible. Attempts to prop up failing businesses, reflate credit, or stimulate consumption only delay the necessary correction and set the stage for the next cycle. Austrian economists frequently point to the boom and bust of the 2000s housing market as a textbook illustration of their theory: the Federal Reserve's historically low interest rates after 2001 created the conditions for an enormous housing boom, and the bust of 2007-2008 was the unavoidable correction.

Murray Rothbard: Anarcho-Capitalism and the Full Austrian Synthesis

Murray Rothbard (1926-1995) was the most controversial and arguably the most creative figure in the post-war Austrian revival. A student of Mises, Rothbard combined Austrian economics with a natural rights political philosophy derived from the American individualist tradition to arrive at a position more radical than any of his teachers: anarcho-capitalism, the complete abolition of the state in favor of voluntary, market-provided institutions.

His major economic work, Man, Economy, and State (1962), is a reconstruction of economic theory from first principles, rigorously developed in the Austrian tradition. Rothbard disagreed with Mises on several points: he was more confident in deriving economic theory from the axiom of human action without any empirical input, and he extended the analysis to show that even a monopoly on money (the central bank) was unjustified on both economic and ethical grounds. Power and Market (published separately in 1970, later combined with Man, Economy, and State) extended this analysis to demonstrate that all government intervention in the economy, including taxation, regulation, and monetary policy, produced outcomes worse than the free market would have delivered.

Rothbard's contribution to libertarian political philosophy is discussed more fully in other articles in this knowledge base. But his economic work is essential for understanding why Austrian economics and libertarianism became so closely linked. The Austrian analysis of markets showed that voluntary exchange generates coordination and prosperity. The Austrian analysis of intervention showed that government action in the economy consistently produces results worse than the problem it was meant to solve. For Rothbard, these were not merely academic points: they were arguments for a radical restructuring of how human beings organize themselves.

The Austrian Revival: From Obscurity to Relevance

By the 1940s and 1950s, the Austrian School was largely marginalized within academic economics. Keynesian economics dominated the profession and the policy world. The Austrians were seen as relics of a pre-mathematical era, their verbal theorizing unable to compete with the elegant models of the neoclassical mainstream. Mises himself had been forced to flee Europe after the Nazi annexation of Austria in 1938, and his position at New York University was unpaid, supported by private funding rather than by the university itself.

The revival began slowly. The publication of Hayek's Road to Serfdom in 1944 made him famous outside academic economics. The founding of the Mont Pelerin Society in 1947, a gathering of free-market thinkers organized by Hayek with participants including Milton Friedman and Karl Popper, created an institutional base for the liberal tradition. The Volker Fund and later the Earhart Foundation provided financial support for Austrian and libertarian research.

The real intellectual revival came after Hayek's Nobel Prize in 1974. The South Royalton conference of 1974, organized by the Institute for Humane Studies, brought together a new generation of economists committed to rebuilding Austrian theory from the ground up. Figures like Israel Kirzner, Ludwig Lachmann, and Murray Rothbard took the Austrian tradition in somewhat different directions: Kirzner emphasized entrepreneurship and market process as the mechanism by which markets tend toward equilibrium, Lachmann emphasized radical uncertainty and the difficulty of knowing whether markets actually do coordinate successfully, and Rothbard pushed the political implications toward anarchism.

Israel Kirzner and the Entrepreneurial Market Process

Israel Kirzner (born 1930) contributed the most important development in Austrian economics in the second half of the twentieth century: the theory of the entrepreneur as the driving force of the market process. Kirzner's entrepreneur is not primarily an innovator in the Schumpeterian sense. He is an alert individual who notices opportunities that others have missed: a price discrepancy between two markets, a resource that could be used more productively, a consumer need that is not being met.

This alertness is precisely what markets reward and bureaucracies punish. The entrepreneur who spots an opportunity and acts on it earns a profit. The profit signal tells him he was right; it tells others that there was an opportunity there; it invites others to compete; and through that competition, the opportunity is eventually arbitraged away and prices move closer to their equilibrium values. This process of entrepreneurial discovery is what moves markets toward coordination without anyone directing it.

Government regulation, in Kirzner's framework, works directly against this process. Every regulation restricts the range of actions that entrepreneurs can take. Every price control prevents prices from signaling the true state of supply and demand. Every subsidy distorts the profit-loss signals that guide entrepreneurial activity. The cumulative effect is that fewer opportunities are discovered, fewer coordination failures are corrected, and the market process works less well than it otherwise would.

Austrian Economics and the Libertarian Movement

The relationship between Austrian economics and libertarianism is not accidental. The Austrian analysis provides a rigorous, non-moralizing argument for why free markets work better than centrally directed economies. You do not need to believe in natural rights or self-ownership to find the Austrian argument compelling. You simply need to accept that knowledge is dispersed, that prices are information, that profit and loss are feedback mechanisms, and that no central authority can know enough to plan an economy successfully.

This made Austrian economics particularly valuable to libertarians who wanted to make policy arguments in a language that secular, empirically minded audiences would find credible. Rothbard combined it with natural rights theory. Hayek combined it with a more pragmatic classical liberalism. Friedman (who was not an Austrian, but admired much of what the Austrians did) combined it with empirical monetarism. The Austrian core, the insistence that markets are knowledge-processing mechanisms that no government can replicate, was broad enough to support multiple political positions within the broadly libertarian family.

The Mises Institute, founded in 1982 in Auburn, Alabama, became the primary institutional home of the Austrian School in the United States. It publishes the scholarly journal Quarterly Journal of Austrian Economics, hosts academic conferences, maintains an enormous online library of Austrian texts, and produces educational content for a broad audience. It has been particularly influential in introducing young people to Austrian ideas and to libertarianism more broadly.

Criticisms of the Austrian School

The Austrian School has not lacked for critics. The mainstream economics profession has largely rejected Austrian methodology on the grounds that it is insufficiently empirical. Economists trained in the neoclassical tradition find the Austrian insistence on verbal theorizing, the rejection of mathematical models, and the skepticism toward econometrics difficult to accommodate. If you cannot test your theory against data, the mainstream argument goes, how do you know whether it is true?

Austrian economists respond in several ways. First, they argue that the fundamental laws of economics, because they are derived from the logical structure of human action, cannot be tested in the way that physical laws can. You cannot run a controlled experiment on an economy. Second, they argue that mainstream econometrics suffers from its own severe limitations: data is always the product of complex historical circumstances, and the identification strategies used to draw causal inferences from it are themselves subject to theoretical assumptions that are rarely made explicit. Third, they point to the track record: the Austrian prediction that intervention creates distortions has been validated repeatedly in historical experience, even if the specific magnitudes cannot be precisely calculated.

The Austrian business cycle theory has been criticized for predicting that recessions should be allowed to liquidate malinvestments without intervention, a prescription that most people find politically unacceptable and potentially cruel. Keynesians argue that Hoover's and Roosevelt's attempts to let the Depression liquidate naturally in the early 1930s proved catastrophic and that the New Deal stimulus helped. Austrians reply that the Depression was largely caused by the Federal Reserve's credit expansion in the 1920s, that Hoover's actual policies were far from laissez-faire, and that the New Deal prolonged the Depression by preventing the necessary adjustments in wages, prices, and business structures.

The Austrian Legacy

Whatever one thinks of the debates over methodology and policy, the Austrian School's core contributions to economic thought are substantial and enduring. The subjective theory of value is now standard across all schools. The theory of capital structure and time preference has influenced economists well outside the Austrian tradition. The socialist calculation argument has never been satisfactorily answered by defenders of central planning. Hayek's knowledge problem remains one of the most powerful arguments against technocratic governance ever made.

For libertarians specifically, Austrian economics provides something of immense value: a systematic account of why markets work and why intervention fails that does not depend on assuming that everyone is selfish or that the world is already in equilibrium. It is a theory of the market as a process, messy and imperfect and constantly changing, but driven by genuine signals and real information in a way that no planned economy can match.

The Austrian tradition is alive today in the work of economists like Peter Boettke, Steven Horwitz, Randall Holcombe, and many others who are carrying the tradition forward while engaging seriously with mainstream economics. Their work suggests that Austrian insights about entrepreneurship, capital theory, and institutional economics are not simply curiosities from the fringes. They are contributions that the economics profession as a whole would be wise to take seriously.