The modern American consumer faces a structural squeeze. Over the last several decades, the cost of core services essential for upward economic mobility: housing, healthcare, and higher education: has risen at a rate that dramatically outpaces wage growth and general price inflation. While technology, global trade, and market competition have successfully lowered the real cost of consumer goods, electronic devices, and apparel, the expenses associated with living in a safe neighborhood, receiving medical treatment, and acquiring professional training have grown prohibitively high.

This divergence is not a natural feature of market economies. It is the direct consequence of a specific pattern of government intervention. In housing, healthcare, and higher education, state and federal policies have systematically subsidized demand while artificially restricting supply. By pumping trillions of dollars of subsidized credit and tax incentives into these markets while legally blocking new construction, licensing new practitioners, and restricting alternative providers, the state has created a persistent scarcity. In this environment, subsidies do not make services more accessible; they are captured by incumbent sellers, driving up prices and trapping consumers in a cycle of debt and dependency.

The Mechanics of Rising Costs in the United States

To address the cost of living crisis, we must examine the unique regulatory and financial dynamics that govern each of these three critical sectors: housing, healthcare, and higher education.

1. Housing: Zoning, NIMBYism, and Credit Inflation

The affordability of housing is dictated by the interaction of local land use regulations and federal monetary and financial policies. The primary driver of rising housing costs in productive metropolitan areas is the artificial restriction of supply through local zoning laws.

Throughout the twentieth century, American municipalities transitioned from flexible, market-responsive development systems to highly restrictive, single-family residential zoning codes. These laws mandate large minimum lot sizes, restrict building heights, outlaw multi-family structures (such as duplexes and apartments), and impose costly parking minimums. By making density illegal, local governments prevent developers from building housing that matches the growth in population and job opportunities.

This supply restriction is reinforced by administrative hurdles, including environmental impact reviews (such as the California Environmental Quality Act at the state level, and the National Environmental Policy Act at the federal level) and planning commission approvals. These statutes require developers to complete extensive environmental impact reports, which can cost hundreds of thousands of dollars and take years to finalize.

NIMBY groups and local homeowners have successfully weaponized these environmental reviews. They file lawsuits to delay construction based on factors such as shadow analysis (arguing a new multi-family building will block solar access to surrounding yards), traffic congestion, aesthetic consistency, and noise pollution. By extending the litigation period, these reviews impose carrying costs (interest on construction loans, property taxes) that can make projects financially unviable, forcing developers to abandon them. This litigation threat serves as a de facto tax on density, protecting property values for existing owners while pricing out new residents.

While local regulations choke supply, federal policies continuously inflate demand. Through government-sponsored enterprises (Fannie Mae and Freddie Mac), federal agencies guarantee trillions of dollars in mortgages, transferring the default risk from private lenders to taxpayers. This federal backstop, combined with central bank credit expansion, lowers borrowing costs and encourages buyers to take on higher levels of leverage.

This government-sponsored system has deep historical roots, beginning with the creation of the Federal National Mortgage Association (Fannie Mae) during the New Deal in 1938, and the Federal Home Loan Mortgage Corporation (Freddie Mac) in 1970. In 1968, Fannie Mae was converted into a stockholder-owned corporation to remove its debt from the federal budget, establishing a model of privatized profits and socialized losses. By purchasing mortgages from private originators, packaging them into mortgage-backed securities (MBS), and guaranteeing their principal and interest, these enterprises removed the risk of default from the banks that issued the loans. Private banks, secure in the knowledge that they could sell their loans to Fannie and Freddie, abandoned strict underwriting standards. This moral hazard culminated in the Subprime Mortgage Crisis of 2008, when the federal government was forced to place both enterprises into conservatorship, committing hundreds of billions of taxpayer dollars to bail them out.

When demand is continuously inflated by cheap credit while supply is legally capped by zoning codes, the economic result is straightforward: prices rise to absorb the new credit. Federal credit subsidies do not help low-income buyers acquire homes; they simply bid up the price of the existing, limited housing stock, enriching current property owners at the expense of renters and young families.

2. Healthcare: The Third-Party Payer Trap and Licensing Cartels

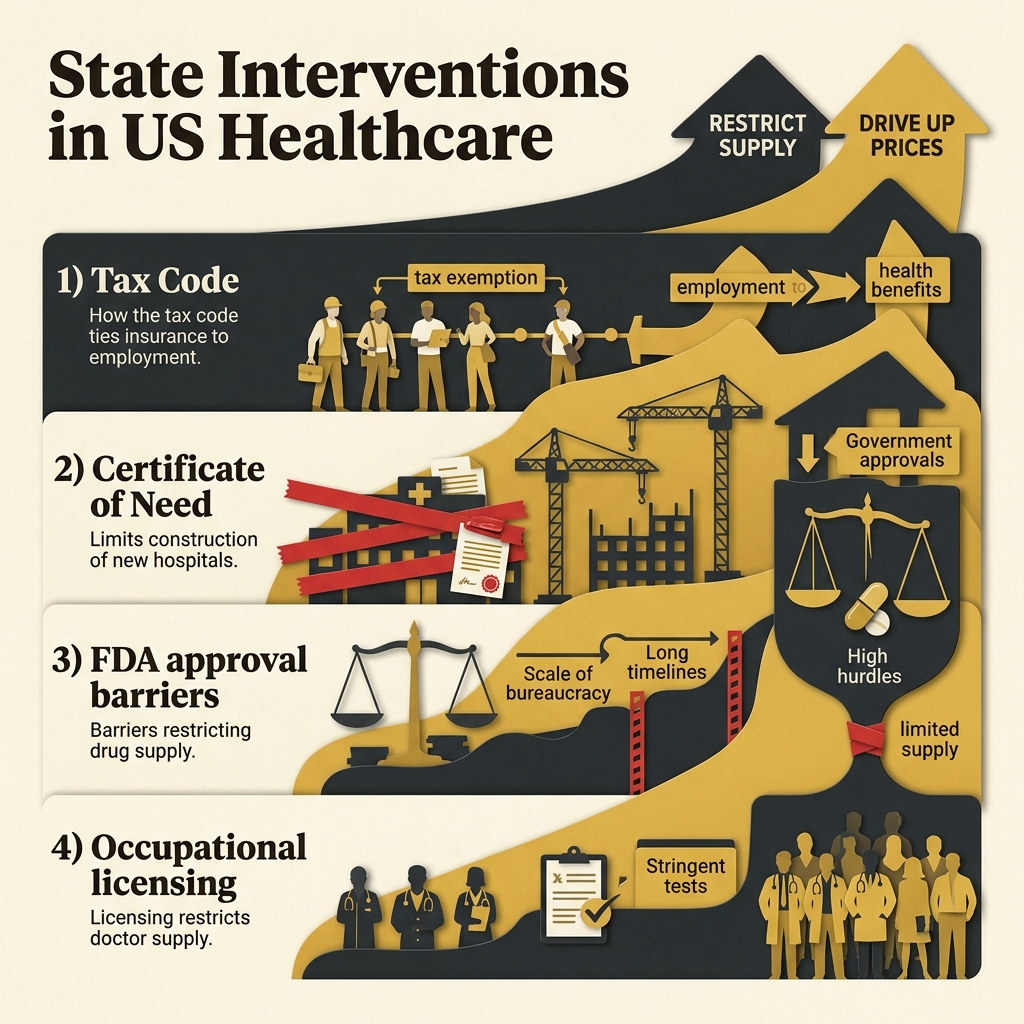

The American healthcare crisis is characterized by explosive cost growth and administrative complexity. The root of this inefficiency is the third-party payer problem, which was established during World War II when the federal government imposed wage controls on private employers. To attract workers without violating wage caps, companies began offering health insurance as a tax-exempt fringe benefit.

In 1954, Congress codified this tax exclusion for employer-sponsored health insurance. This policy created a massive distortion: it incentivized employees to receive their compensation in the form of comprehensive health insurance plans rather than cash wages. Over time, health insurance transitioned from a catastrophic shield (designed to cover unexpected, ruinous events) into a pre-paid administrative system that covers routine, predictable maintenance (such as annual physicals, dental cleanings, and prescription drugs).

The employer tax exclusion is also a highly regressive subsidy. Because the tax savings are tied to an individual's marginal tax rate, high-income earners in top tax brackets receive a much larger discount on health insurance than low-income workers in lower brackets. This distortion encourages high-earning professionals to demand gold-plated insurance plans with zero deductibles and expansive coverage, driving up administrative costs. At the same time, because employers must cover these premium hikes to maintain benefits packages, they offset the cost by suppressing cash wages. Over the last four decades, the stagnation of middle-class cash wages in the United States is directly correlated with the rising cost of employer-sponsored health benefits, as the tax-sheltered compensation is captured by healthcare administrators and insurance intermediaries.

This transition broke the direct pricing relationship between the patient (the consumer) and the doctor (the provider). In an autonomous market, consumers shop for value, forcing providers to compete on price, quality, and efficiency. Under the third-party payer model, the patient does not know the price of treatment, and the provider does not disclose it, as both interact through insurance intermediaries or government agencies (Medicare and Medicaid). This insulation eliminates the price awareness that drives cost-efficiency in other industries, leading to over-consumption and administrative expansion.

To protect this high-cost structure, the state restricts medical supply through several regulatory cartels:

- Certificate of Need (CON) Laws: In many states, medical providers cannot build new clinics, open imaging centers, or purchase advanced diagnostic equipment without first securing permission from a state board. These boards are typically dominated by representatives from existing, incumbent hospitals who use the process to block new competitors from entering the market.

This regulatory barrier is particularly damaging in rural and underserved areas. When a private clinic attempts to purchase a magnetic resonance imaging (MRI) machine or open an urgent care center to compete with a hospital monopoly, the hospital's legal team can object at the CON hearing, claiming the local market does not "need" another provider. This legal process can take months and cost tens of thousands of dollars in attorney fees, preventing capital from entering the market to lower prices and expand care. - Medical Licensing Restrictions: State licensing boards, under the influence of medical associations, restrict the supply of healthcare workers. They limit the number of medical school admissions, impose barriers on foreign-trained doctors, and restrict the scope of practice for nurse practitioners and physician assistants, preventing them from providing routine care without expensive physician supervision.

This supply constraint has historical roots in the Flexner Report of 1910. Commissioned by the American Medical Association (AMA) and funded by the Carnegie Foundation, the report recommended raising licensing standards and shut down over half of the existing medical schools in the United States, particularly those that trained low-income and minority practitioners. By centralizing control over medical education and licensure, the AMA created a protected cartel. Over the subsequent century, this restriction has kept physician salaries artificially high and limited the total supply of practitioners, leaving the public to face long wait times and high fees. - FDA Approvals and Patent Monopolies: The Food and Drug Administration's approval process for new pharmaceuticals and medical devices requires hundreds of millions of dollars and takes over a decade. While safety testing is necessary, the extreme cost and length of the process protect large, incumbent pharmaceutical companies from competition, while extended patent protections grant them monopoly pricing power over life-saving medications.

The high cost of FDA compliance prevents smaller research laboratories and generic drug manufacturers from entering the market. Furthermore, major pharmaceutical firms engage in "patent evergreen" strategies, making minor changes to a drug's formula (such as switching from a tablet to a capsule) to extend their monopoly rights for another twenty years. This regulatory protection shields large drug firms from generic competition, allowing them to charge monopoly prices that are subsidized by taxpayers through Medicare and private insurance.

3. Higher Education: Subsidies and Administrative Bloat

The rise in college tuition represents a classic case of the Bennett Hypothesis in action. Formulated by former Secretary of Education William J. Bennett in 1987, this hypothesis states that increases in federal financial aid enable higher education institutions to raise their tuition rates, capturing the government subsidy for themselves.

The Higher Education Act of 1965 established the framework for federal student loan programs. Over the subsequent decades, the federal government took control of the student loan market, offering low-interest loans directly to students regardless of their field of study, credit history, or probability of graduation. Because these loans are backed by the federal government and are legally exempt from normal bankruptcy discharge rules, universities face no financial risk when admitting students who borrow heavily.

With a guaranteed stream of federal funding, colleges and universities are insulated from the discipline of the market. Instead of competing on the quality and affordability of instruction, institutions began competing on non-academic amenities to attract students: luxury student housing, dining halls, recreation facilities, and athletic programs.

More importantly, this subsidization fueled massive administrative bloat. Since the 1970s, the number of administrators and professional staff at American universities has grown at a rate that is double or triple the rate of student enrollment and faculty hiring. Universities have built large bureaucracies dedicated to compliance, diversity programs, student life, marketing, and institutional advancement. Because the federal government pays the bill through student debt, universities simply raise tuition rates to fund this growing overhead, leaving students with lifelong debt burdens.

This cheap credit influx has also caused severe credential inflation in the labor market. As federal subsidies enabled a massive expansion in the number of college graduates, a bachelor's degree ceased to function as a signal of elite academic capability or specialized technical skill. Instead, it became a basic sorting mechanism for employers. To filter the large pool of applicants, businesses began demanding a college degree for entry-level administrative, clerical, and customer service positions that historically only required a high school diploma.

This shift forces young people to attend college and borrow heavily, not because they need higher-order training to perform the job, but simply to secure a credential that grants them entry into the white-collar workforce. This credentialism acts as a regressive barrier to upward mobility. It forces low-income individuals to take on ruinous debt for low-value degrees, or remain locked out of the primary job market, while the university cartel captures the subsidized cash.

This growth in administrative overhead is driven by state and federal regulatory compliance mandates. To participate in federal student aid programs under Title IV of the Higher Education Act, colleges must maintain extensive compliance departments. They must comply with complex reporting requirements, Title IX investigations, campus security audits, and financial aid processing protocols. For a traditional college, this compliance overhead requires hiring hundreds of non-teaching personnel, diverting tuition revenue from instruction to administrative management.

This system is protected by regional accreditation monopolies. The federal government restricts student aid eligibility to institutions accredited by a small number of private, peer-review organizations. These accrediting bodies are dominated by existing traditional universities, which use the process to block low-cost online providers, vocational schools, and alternative certification programs from entering the higher education market, preserving the traditional university cartel.

The accreditation process functions as a barrier to entry by requiring new providers to emulate the high-overhead model of traditional colleges. To receive accreditation, a new provider must typically possess a physical campus, maintain a traditional library, employ a set percentage of full-time PhD faculty, and show significant financial reserves. These rules prevent low-cost digital education providers, specialized bootcamps, and apprenticeships from competing for students on equal footing, shielding traditional universities from competitive price pressures.

A Practical Program for Rolling Back Interventions

To restore affordability, we must systematically dismantle the regulatory structures that subsidize demand and restrict supply across housing, healthcare, and higher education.

1. Housing: Upzoning, By-Right Development, and Financial Rollbacks

The rollback of housing restrictions requires a shift in land-use authority away from local planning commissions toward a system governed by property rights:

- State-Level Preemption of Local Zoning: State legislatures should pass laws that override restrictive local zoning codes. These reforms must establish absolute "by-right" development, meaning that if a proposed building complies with basic safety and building codes, the local planning commission cannot block it or delay it through public hearings.

- Eliminating Density Caps: Localities must be prohibited from mandating single-family zoning, minimum lot sizes, and parking minimums. Property owners should be free to convert single-family homes into duplexes, triplexes, or accessory dwelling units (ADUs), and to build high-density multi-family housing in commercial zones without special permits.

- Streamlining Environmental Reviews: Environmental protection laws must be amended to prevent NIMBY litigators from using the review process as a tool to delay or block urban housing developments. Environmental reviews should be restricted to actual, physical environmental impacts, rather than aesthetic, parking, or traffic concerns.

- Winding Down Federal Guarantees: The federal government must phase out Fannie Mae and Freddie Mac, transitioning the mortgage market to private lenders who must assess and price risk without taxpayer backing. This rollback will cool demand by ending the artificial inflation of the mortgage credit supply.

A transition to private mortgage-backed securities (MBS) markets will require private lenders to bear the full cost of default risk. Without a government backstop, banks will be forced to raise lending standards: requiring higher credit scores, verifying employment and income, and demanding substantial down payments (typically twenty percent). While this may reduce the initial volume of mortgage originations, it will cool housing demand, stopping the credit-fueled bidding wars that inflate property prices. The market will stabilize around realistic valuations determined by real savings rather than taxpayer-subsidized debt, making home purchases affordable in the long run.

2. Healthcare: Repealing CON Laws, Restoring First-Party Pricing, and Deregulating Insurance

Restoring affordability to healthcare requires returning patients to their role as first-party shoppers:

- Abolishing Certificate of Need (CON) Laws: State governments should immediately repeal all CON laws, allowing anyone to build healthcare facilities, open specialty clinics, or purchase diagnostic equipment without government permission.

- Expanding Scope of Practice: State medical boards must eliminate restrictions on nurse practitioners and physician assistants, permitting them to open independent practices, prescribe routine medications, and diagnose common illnesses without physician supervision.

- Nationalizing the Insurance Market: The federal government should eliminate state-level insurance mandates and allow insurers to sell policies across state lines. This reform will create a competitive national market for insurance, driving down premiums and encouraging the development of low-cost, catastrophic-only plans.

- Equalizing the Tax Treatment of Healthcare: The tax exclusion for employer-sponsored health insurance must be phased out, or equalized by offering a matching tax deduction for individual, out-of-pocket healthcare savings and insurance purchases. This change will encourage individuals to purchase portable insurance plans directly, breaking the link between employment and healthcare and encouraging a return to direct pricing.

- Deregulating the FDA and Lifting Drug Import Bans: The federal government should permit the immediate importation of pharmaceuticals and medical devices that are already approved by trusted international regulators, such as the European Medicines Agency (EMA) in Europe or the PMDA in Japan. By establishing a system of regulatory reciprocity, foreign generic manufacturers can enter the US market immediately, breaking the domestic patent monopolies and lowering drug costs through direct competition.

3. Higher Education: Phasing Out Loans and Ending Accrediting Monopolies

Reforming higher education requires ending the guaranteed flow of subsidized federal credit:

- Phasing Out Federal Student Loans: The federal government must wind down the direct student loan program, forcing higher education financing back into the private sector. Private banks and credit unions will be forced to assess the creditworthiness of borrowers and the expected return on investment of specific fields of study, ending the funding of low-utility degrees.

By forcing higher education funding into private debt markets, this reform will automatically redirect students toward vocational and technical training. Because private lenders must evaluate the probability of repayment, they will offer lower interest rates for programs with high market demand: such as mechanical engineering, nursing, plumbing, or software development: while charging high premiums or refusing to lend for low-value degrees. This pricing mechanism will discourage students from spending four years acquiring credentials of low economic utility, and instead encourage them to enter two-year technical schools, coding bootcamps, and employer-sponsored apprenticeship programs that offer a direct, affordable pathway to employment without the high administrative overhead of traditional universities. - Restoring Normal Bankruptcy Rights: Congress must repeal the special exemption that prevents student loans from being discharged in bankruptcy. If student loans can be discharged, private lenders will be much more cautious when lending, driving down the overall supply of credit and forcing universities to lower tuition rates to attract students.

- Abolishing Regional Accrediting Monopolies: The Department of Education should recognize alternative, low-cost certification bodies, vocational associations, and online education providers. By allowing new competitors to enter the market, the traditional university cartel will be forced to lower their prices or face obsolescence.

Comparative Analysis of International Systems

To find the best compromise reform frameworks, we must examine the housing and healthcare systems of other nations, analyzing what works and what fails in each.

1. International Housing Models

When looking abroad, two primary models of housing provision stand out: the Singapore Housing and Development Board (HDB) model and the Vienna Social Housing model.

Singapore: The HDB Leasehold and CPF System

Singapore’s housing market is a unique hybrid system. The state owns approximately 90 percent of the land and builds the majority of the housing stock through the Housing and Development Board (HDB). Roughly 80 percent of Singapore's resident population lives in HDB flats.

Citizens do not own HDB flats in perpetuity; they purchase 99-year leases. These leases can be bought and sold on a regulated secondary market, allowing citizens to build equity and accumulate wealth. This purchase is financed by the Central Provident Fund (CPF), a mandatory social security savings scheme where employees and employers must contribute a portion of wages into individual accounts that can be drawn down to fund home purchases.

The advantage of the Singapore model is its high homeownership rate (over 85 percent) and the avoidance of the slum-like conditions associated with social housing in the West. By coupling mandatory individual savings with long-term leasehold assets, Singapore has built a stable property market without the fiscal burden of massive tax-funded welfare subsidies.

However, the system carries severe libertarian liabilities. It relies on a state monopoly of land ownership, which restricts the development of a free private property market. The government also uses housing allocation to enforce ethnic quotas and social engineering. Furthermore, the mandatory nature of the CPF scheme represents a form of forced savings that deprives individuals of the freedom to manage their own capital.

This mandatory savings requirement is a significant distortion. Employees must divert up to 20 percent of their wages, and employers must contribute an additional 17 percent, into the CPF. This high contribution rate restricts the cash wages available to workers, limiting their capacity to allocate their savings to other investments, start private businesses, or fund immediate consumption choices.

Furthermore, the 99-year leasehold system creates a ticking retirement problem. As the leases on older HDB flats near their end, the market value of these properties will decline toward zero, eroding the household wealth that citizens were forced to accumulate in their homes.

Vienna: The Municipal Social Housing Model

Vienna’s housing system relies on municipal ownership and rent control. The city government owns approximately 220,000 housing units directly, and subsidizes another 200,000 units managed by limited-profit housing associations. Over 60 percent of Vienna's population lives in social housing.

The system is funded by a corporate and individual income tax surcharge, which is pooled to build and maintain municipal housing. Rent prices are set by the city government, and income eligibility rules are highly generous, meaning that the middle class lives in social housing alongside low-income residents.

While the Vienna model has kept rental costs low for current tenants, it suffers from the classic inefficiencies of price controls. Because rents are artificially depressed, the market does not clear, leading to long waiting lists for municipal flats.

This price depression leads to housing decay, as municipal governments and limited-profit developers do not face market incentives to maintain buildings efficiently or upgrade facilities. It also creates a black market for subleasing, where tenants who hold historical, low-rent leases sublet their apartments to newcomers at market rates, pocketing the difference.

The system is also fiscally expensive, requiring continuous tax subsidies to fund new construction. For libertarians, the model is a dead end: it relies on high taxation, public debt, and the elimination of private landlords, preventing the price mechanism from signaling resource scarcity.

2. International Healthcare Models

In healthcare, we can compare Singapore's 3M model with Switzerland's universal private insurance system.

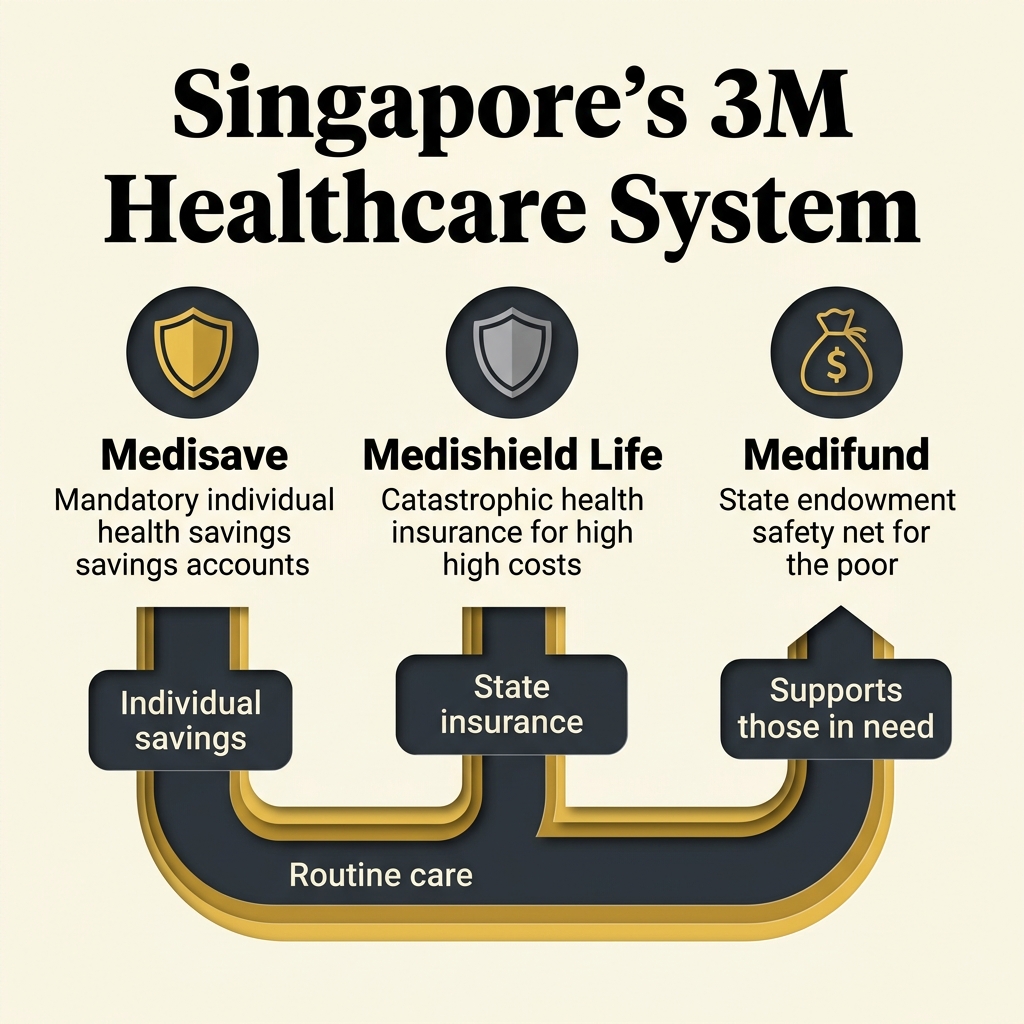

Singapore: The 3M Model

Singapore's healthcare system is built on three pillars, collectively known as the 3Ms:

- MediSave: A mandatory medical savings account. Employees must contribute between 7 and 9.5 percent of their wages (depending on age) into their personal MediSave account. These funds can only be used to pay for personal or immediate family medical expenses.

- MediShield Life: A universal, catastrophic health insurance plan. This plan has high deductibles and co-payments, and is designed to cover large hospital bills and expensive treatments like chemotherapy.

- MediFund: A government-funded safety net. If a citizen's MediSave and MediShield accounts are exhausted, and they cannot afford their medical bills, they can apply for assistance from MediFund. The fund is managed by independent committees that assess need on a case-by-case basis (means-testing).

The advantage of the Singapore system is its high cost-efficiency. Singapore spends roughly 4 to 5 percent of its GDP on healthcare, yet achieves health outcomes (life expectancy, infant mortality) that are superior to the United States, which spends over 17 percent of GDP. By relying on MediSave as the primary funding tool, Singapore has preserved first-party pricing for routine care, preventing the third-party payer trap.

This cost-sharing model stands in sharp contrast to universal single-payer models like the National Health Service (NHS) in the United Kingdom. Under the NHS, healthcare is funded through general taxation and provided free at the point of service. Because the consumer price is set to zero, demand is virtually infinite. Since the state cannot raise taxes indefinitely to cover this infinite demand, it is forced to ration care through administrative delays and waitlists. Patients in single-payer systems often wait months for diagnostic imaging, specialist consultations, and non-emergency surgeries, during which their health can decline.

Furthermore, because the government acts as a single monopsony buyer, it imposes price controls on medical equipment, supplies, and salaries. This pricing distortion suppresses medical innovation, drives qualified medical professionals to relocate to countries with higher pay, and results in overcrowded, decaying municipal hospitals. By requiring citizens to use their own savings for routine treatment, Singapore eliminates the artificial demand spike that cripples single-payer systems, ensuring that medical resources are allocated by the price system rather than state rationing queues.

The libertarian critique of Singapore's healthcare focuses on the mandatory savings rate and the extensive state management of the supply side. The government owns the majority of acute care hospitals, regulates the number of medical students and specialists, sets price targets, and maintains a strict formulary that limits which medications are subsidized.

Switzerland: The Mandated Multi-Payer System

Switzerland’s healthcare system is entirely private on the supply side, but highly regulated on the demand side. The state does not run hospitals or provide public insurance. Instead, all residents are legally required to purchase basic health insurance from private, non-profit insurance companies.

The government regulates the basic insurance package, ensuring that insurers cannot deny coverage for pre-existing conditions or charge different premiums based on health risk (community rating). To make this mandate affordable, the state provides subsidies to low-income individuals to help them pay their premiums.

These premium subsidies are managed at the cantonal (provincial) level, creating public choice distortions. Cantonal governments determine the income thresholds for subsidies and pay them directly to insurers on behalf of eligible citizens. Because these subsidies are funded through general cantonal tax revenues, local politicians have a strong incentive to manipulate eligibility criteria to capture voting coalitions. In wealthy cantons, eligibility thresholds are set high enough to cover significant portions of the middle class, turning a targeted safety net into an expansive middle-class entitlement. This administrative expansion increases the cantonal tax burden, introduces political rent-seeking into the insurance market, and shields a growing segment of the population from the true cost of health services, distorting the market's efficiency.

This community-rating requirement creates significant market distortions. Because insurers are barred from pricing premiums based on actual individual health risks, healthy individuals are forced to subsidize high-risk individuals. To prevent insurers from selectively recruiting only healthy clients (cherry-picking), the Swiss government administers a complex risk-equalization pool. Insurers that attract healthier-than-average clients are forced to pay cash into the pool, which is then distributed to insurers with sicker-than-average clients. This administrative intervention destroys the pricing of risk and replaces competitive insurance underwriting with government-managed risk transfers.

Furthermore, the Swiss system is expensive, with healthcare spending accounting for over 11 percent of GDP. While the system avoids waitlists, Swiss families face high premiums and substantial out-of-pocket costs due to high statutory deductibles (known as franchises) and co-payments. For libertarians, the mandatory purchase requirement is a form of coercion, and the heavy regulation of insurance packages restricts consumer choice and prevents insurers from offering customized, low-cost plans.

The Compromise Libertarian Reform Framework

Based on our analysis of the US crisis and international systems, we can formulate a set of compromise reforms. These reforms acknowledge political realities: such as the public demand for basic safety nets: but implement them through mechanisms that preserve the price system, property rights, and voluntary association.

1. Housing Compromise: Public Trust Land Banking with By-Right Building Codes

A politically viable compromise for housing reform must address the state's role in planning while restoring private property rights:

Instead of municipal zoning boards micro-managing land use (deciding exactly what can be built on every plot), municipalities can establish a public-trust land bank model. The local government focus is restricted entirely to structural planning: defining where public infrastructure (roads, sewers, parks, transit lines) will be built.

On top of this structural planning, the land use code must be completely deregulated. Property owners have an absolute by-right entitlement to build any density (single-family, duplexes, multi-family apartment buildings, commercial developments) on their land, provided the structure meets basic safety codes. Planning commissions and NIMBY neighborhood groups are stripped of their power to block projects or delay approvals.

To address the need for low-income housing, the state can permit the creation of private, non-profit community land trusts. These trusts can purchase land and hold it in common, leasehold structures, similar to the Singapore HDB model. This allows low-income families to purchase the equity of the home itself at a low cost, while the trust preserves the land for long-term community use, avoiding the tax-funded bureaucracy of public housing.

Furthermore, the coordination of local neighborhood amenities and aesthetic standards can be managed through private covenants and homeowners' associations (HOAs). In a free-market framework, HOAs represent voluntary contract-based associations where buyers choose to agree to specific neighborhood rules. Unlike municipal zoning, which is enforced by state coercion on all residents, private covenants are governed by civil contract law, allowing different communities to offer different styles of living in a competitive market.

This voluntary covenant model has been successfully demonstrated in master-planned communities like Reston, Virginia and Columbia, Maryland. These communities were designed by private developers who laid out the structural plans (roads, utilities, green spaces, commercial centers) in advance and established private deed restrictions to maintain architectural consistency and coordinate common amenities.

Because these associations are governed by private contract rather than public administrative law, they must respond to the preferences of buyers. If a homeowners' association imposes rules that are too restrictive, property values decline as buyers choose to move to competing developments with more flexible covenants. By shifting land use governance from coercive city councils to competing, contract-based private associations, the housing market can coordinate complex community planning while fully preserving individual liberty.

2. Healthcare Compromise: Delinking, HSA Vouchers, and Mutual Aid

An ideal libertarian compromise for healthcare must replace the high-cost third-party payer model with a system centered on personal Health Savings Accounts (HSAs) and catastrophic insurance:

First, we must delink health insurance from employment by eliminating the tax exclusion for employer-sponsored plans and replacing it with a universal health tax deduction available to all individuals. This will encourage the growth of a portable, competitive individual insurance market where plans travel with the worker.

Second, the state should transition public health programs (Medicaid and Medicare) away from direct service provision and administrative rate-setting. Instead, these programs must be transformed into a system of means-tested HSA vouchers. The state provides low-income and elderly citizens with a direct, monthly voucher deposit into their personal HSA.

The HSA funds belong to the individual and can only be spent on medical services or private catastrophic insurance premiums. Under this system, even the poorest citizens act as first-party shoppers. Because they control the money in their HSA, they have a direct incentive to shop for affordable care and ask for transparent pricing, driving cost competition among providers. Doctors will be forced to compete for these voucher dollars by offering transparent, upfront pricing.

To maximize the effectiveness of this compromise, the regulatory definition of allowable HSA expenditures must be significantly deregulated. Currently, federal tax rules restrict HSA usage to traditional, state-licensed medical procedures and prescription drugs. Under a libertarian compromise framework, individuals should be permitted to spend their HSA funds on any service or product related to their personal health and wellness. This includes nutritional counseling, gym memberships, physical therapy, alternative medicine, non-prescription supplements, and preventative fitness programs. By allowing HSAs to cover a broad spectrum of preventative health choices, individuals are empowered to take proactive responsibility for their well-being, reducing their dependency on the high-cost, intervention-oriented medical cartel and lowering overall healthcare demand in the long run.

A key element of this transition is the expansion of the Direct Primary Care (DPC) model. Under DPC, patients pay their primary care doctor a flat, monthly membership fee (typically between 50 and 100 dollars) directly, bypassing the insurance billing apparatus. DPC clinics do not accept insurance, which eliminates the administrative overhead associated with insurance coding and collections: overhead that accounts for up to 40 percent of a typical medical clinic's operating costs.

By eliminating this billing bureaucracy, DPC doctors can offer unlimited office visits, direct communication, and wholesale prices on lab tests and prescriptions, making routine healthcare highly affordable and accessible without third-party intervention.

Third, we must encourage the restoration of mutual aid friendly societies. By removing legal restrictions that prevent fraternal organizations, churches, and mutual aid networks from pooling funds to provide cooperative healthcare and primary care doctor contracts (the lodge-doctor model), civil society can rebuild affordable safety nets that bypass the corporate insurance state.

Conclusion: The Path to a Voluntary Society

The modern cost of living crisis in housing, healthcare, and higher education is the predictable outcome of demand subsidization coupled with supply restriction. The solution is not to double down on state-funded welfare or impose price controls, which merely exacerbate scarcity and create waiting lists. This pattern of subsidizing scarcity has created a corporate welfare state that benefits entrenched administrative and corporate cartels at the expense of productive individuals.

To break this cycle, the movement for liberty must offer solutions that are both theoretically sound and politically actionable. We must explain that true compassion does not consist in the state guaranteeing services through coercive taxation and inflation, which inevitably leads to quality degradation and administrative rationing. Real compassion is found in the liberation of the supply side, allowing the price mechanism and free competition to drive costs down and quality up, as they have done in every unregulated sector of the economy.

Instead, we must implement a dual strategy of deregulation and market-oriented compromises. By stripping local planning boards of their zoning power, ending the federal subsidization of higher education, and transforming public health programs into personal HSA vouchers, we can restore the price signals that coordinate economic activity.

These reforms represent a practical bridge to a free society. They protect the vulnerable through direct, means-tested purchasing power, while ensuring that the actual provision of housing, healthcare, and education is governed by free competition, property rights, and voluntary association. By transitioning from the corporate welfare state to a libertarian framework, we can make the core necessities of economic mobility accessible, high-quality, and affordable for all.