Capital markets are the primary nervous system of a modern economy. They do not merely facilitate the buying and selling of financial assets; they coordinate the allocation of scarce resources across time. Through the pricing of risk, debt, and equity, capital markets align the immediate consumption choices of savers with the long-term investment projects of entrepreneurs. When functioning autonomously, this system directs capital toward its most value-productive uses, raising the marginal productivity of labor, lowering consumer prices, and driving sustainable economic expansion.

However, capital markets do not operate in a vacuum. The state continuously intervenes in this coordination process through three main vectors: monetary inflation, fiscal taxation, and administrative regulation. While these interventions are often promoted under the guise of stabilizing markets, funding public goods, or protecting consumers, they systematically disrupt the price signals that guide capital accumulation and distribution. The result is a divergence between the short-run illusions of prosperity and the long-run realities of capital depletion, structural distortion, and wealth polarization.

The Structural Nature of Capital and Time Preference

To analyze the impact of government intervention on capital markets, one must first reject the view that capital is a homogeneous, self-reproducing blob. In classical and Austrian economic theory, capital is recognized as a complex, highly specific, and heterogeneous structure of physical assets: factories, machinery, tools, raw materials, and half-finished goods. These capital goods are arranged in vertical stages of production, ranging from early stages (research, mining, exploration) to final stages (retail, distribution, consumption).

This structure of production is coordinated by time preference: the degree to which individuals value immediate satisfaction over future satisfaction. Time preference determines the natural rate of interest. If individuals have a low time preference, they choose to save a higher portion of their income, deferring immediate consumption. This increase in savings expands the supply of loanable funds, lowering interest rates and signaling to entrepreneurs that consumer demand is being deferred. Entrepreneurs can then borrow these savings to invest in long-term, roundabout stages of production, secure in the knowledge that the physical resources (labor, capital goods) required to complete these projects have been freed up by the corresponding drop in consumer spending.

This coordinating mechanism is illuminated by Carl Menger's pioneering classification of goods by orders. First-order goods are consumer goods that directly satisfy human desires, such as bread or clothing. Second-order goods, such as flour or leather, are used to produce first-order goods. Higher-order goods, such as agricultural machinery, wheat fields, or research laboratories, are further removed from final consumption.

Eugen von Böhm-Bawerk observed that production is inherently time-consuming, and that more roundabout methods of production (those involving higher-order capital goods) are more physically productive. A fisherman catching fish with his bare hands is operating in a first-order, low-productivity process. By taking time to construct a net (a higher-order capital good), he increases his catch rate dramatically. However, to construct the net, he must have saved enough fish in advance to sustain himself during the time he is not fishing. Savings represent the real, physical resources required to sustain labor during the time-interval of roundabout production.

If individuals have a high time preference, they choose to spend their income immediately, saving very little. Interest rates rise, signaling to entrepreneurs that long-term investment projects are not supported by a sufficient pool of real savings. The economy is forced to focus on shorter-term, less roundabout stages of production that yield immediate consumer goods. Under an autonomous price system, interest rates act as a balancing mechanism, ensuring that the time-horizon of investment projects matches the time-horizon of consumer saving.

Monetary Inflation: Credit Expansion and Malinvestment

Monetary inflation: defined as the expansion of the money supply by the central bank and the commercial banking cartel: is the most pervasive intervention in capital markets. Modern central banks do not inflate the currency by printing physical bills and dropping them from helicopters. Instead, they conduct credit expansion by purchasing government debt and financial assets from primary dealers, creating new bank reserves by electronic entry. These reserves are then multiplied through the fractional reserve banking system, lowering nominal interest rates below their natural, time-preference level.

To understand these mechanics, we can analyze the operational tools of modern monetary authorities, such as the Federal Reserve. Through Open Market Operations and modern facilities like overnight reverse repurchase agreements and quantitative easing (QE), central banks purchase massive volumes of treasury securities and mortgage-backed securities directly from primary dealers. By crediting the reserve balances of these financial intermediaries, the central bank floods the interbank market with liquidity. This drives down the overnight benchmark rate, such as the federal funds rate, which in turn compresses yields across the entire yield curve. When the price of short-term and long-term debt is artificially depressed, the pricing of risk is systematically dismantled. The risk premium: the compensation investors demand for holding risky assets over safe assets: vanishes, forcing capital into increasingly speculative markets in search of yield.

This persistent manipulation also fosters financialization: a structural shift where corporations prioritize financial engineering over productive engineering. When the cost of corporate debt is artificially low, companies find it more profitable to issue cheap bonds to fund stock buybacks, leveraged buyouts, and mergers, rather than investing in new capital assets, product R&D, or workforce training. Stock buybacks boost earnings per share in the short run, rewarding executives whose compensation is tied to stock performance, but they deplete the firm's long-term capital reserves. This debt-financed financialization inflates asset bubbles while leaving the real, underlying productive structure of the firm stagnant.

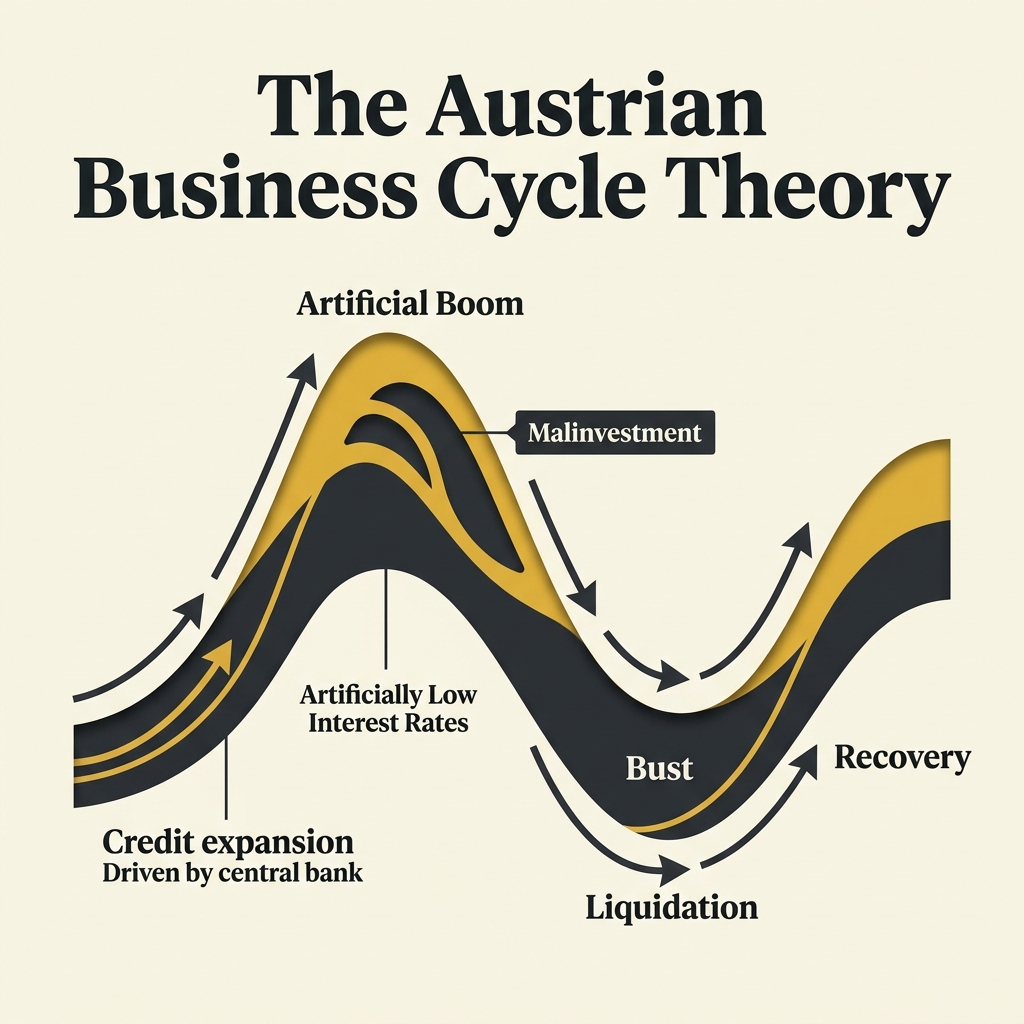

Short-Run Effects: The Artificial Boom

In the short run, credit expansion creates a powerful illusion of prosperity. Because the new money enters the market through credit channels, entrepreneurs see a drop in interest rates and assume that society's savings pool has expanded. They borrow this newly created credit to embark on long-term, highly roundabout investment projects: such as commercial real estate, technology start-ups, and heavy infrastructure: that previously seemed unprofitable.

At the same time, because consumers have not actually reduced their spending, consumer-facing industries remain highly profitable. The result is an artificial boom. Demand for capital goods, raw materials, and labor rises, bidding up prices and wages across the economy. Stock markets, real estate markets, and other asset classes experience rapid price appreciation as the newly created credit flows into financial speculations. This short-run phase is characterized by high levels of risk-taking, low yields, and a general belief that the business cycle has been solved.

However, this boom is structurally unstable. It is not supported by real savings. Real savings represent the physical resources: food, fuel, steel, concrete: that savers chose not to consume, leaving them available for workers to use while completing new investment projects. Credit expansion creates money, but it does not create these physical resources. It merely creates more monetary tickets competing for the same limited pool of resources.

Long-Run Effects: Malinvestment and the Cantillon Effect

In the long run, the structural mismatch between real savings and credit-driven investment becomes manifest. As the new investment projects compete with consumer industries for labor and materials, resource scarcity drives up production costs. Entrepreneurs find that the funds they borrowed are insufficient to complete their projects because the prices of input goods have been bid up.

This phenomenon is not "overinvestment" but "malinvestment": the misdirection of capital into projects that cannot be completed or sustained once the credit expansion stops. When the central bank is eventually forced to halt credit expansion to prevent accelerating price inflation, interest rates rise toward their natural level. The artificial profitability of the roundabout projects evaporates, leading to the bust: a liquidation phase where malinvestments are shut down, asset prices collapse, and labor must be reallocated to sustainable industries.

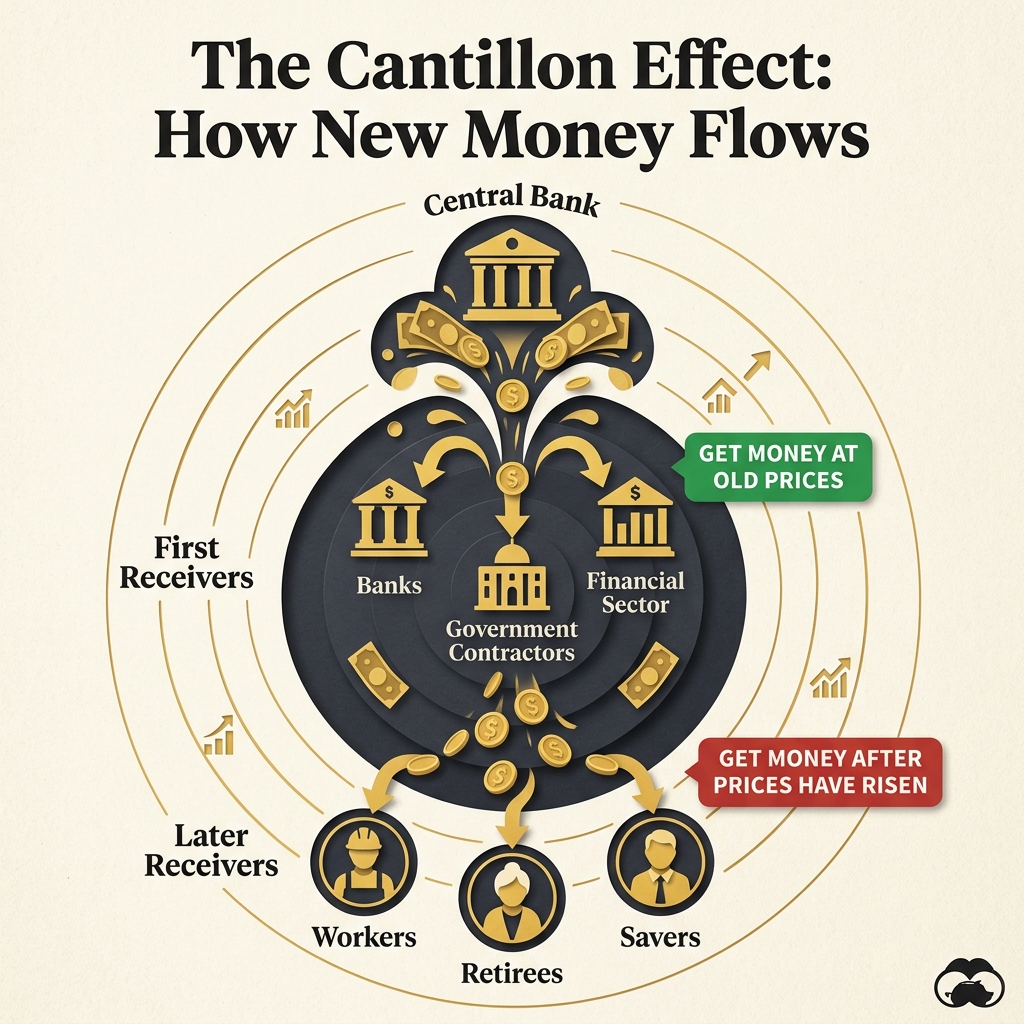

Beyond the business cycle, monetary inflation distorts the distribution of capital through the Cantillon effect. Newly created money is not distributed evenly. The first recipients: the state, large commercial banks, defense contractors, and major financial institutions: receive the money before prices have risen, allowing them to purchase resources and assets at pre-inflation rates.

As this money is spent, it cascades through the economy, bidding up prices. By the time the new money reaches wage earners, retirees, and small businesses at the periphery of the economy, prices have already risen. The Cantillon effect acts as a silent wealth transfer, redirecting capital and purchasing power away from productive savers toward the state and its politically connected financial partners. This permanent wealth redistribution distorts the capital structure, pricing the working class out of asset ownership and encouraging speculative leverage over productive investment.

Additionally, inflation leads to capital consumption. When prices are rising rapidly, historical cost accounting fails to capture the true cost of asset replacement. A firm calculating its profits based on the historical cost of its machinery will overstate its earnings, as the replacement cost of that machinery has risen. As a result, firms pay taxes on phantom profits and distribute dividends that are actually drawn from their capital base, gradually hollow out the economy's productive infrastructure.

This structural hollowing out is particularly clear when comparing capital markets under different monetary standards. In the nineteenth century, the classical gold standard anchored capital markets. Because money had a fixed physical supply that could not be expanded by administrative decree, capital markets were guided by real savings. Investors faced real interest rates that accurately reflected time preference, encouraging long-term capital accumulation and infrastructure investment, such as the massive rail networks and industrial factories of the era. The price level was stable or gently declining, which rewarded savers and discouraged speculative debt. Since the abandonment of the gold anchor in 1971, capital markets have been characterized by extreme volatility, repeating boom-and-bust cycles, and a massive expansion of private and public debt. Debt, rather than savings, has become the primary lubricant of capital allocation, leading to a fragile, highly leveraged corporate structure that requires continuous central bank support to prevent collapse.

Taxation: The Direct Depletion of Savings

If monetary inflation distorts capital prices, taxation represents a direct extraction of capital from the private sector. Every dollar collected in taxes by the state is a dollar that cannot be saved, invested, or used to maintain private capital assets. The state typically justifies taxation as a method to fund infrastructure, education, and social safety nets. However, this transfer replaces market-driven capital allocation with political allocation, altering the incentives that drive capital accumulation.

Short-Run Effects: Profit Compression and Deadweight Loss

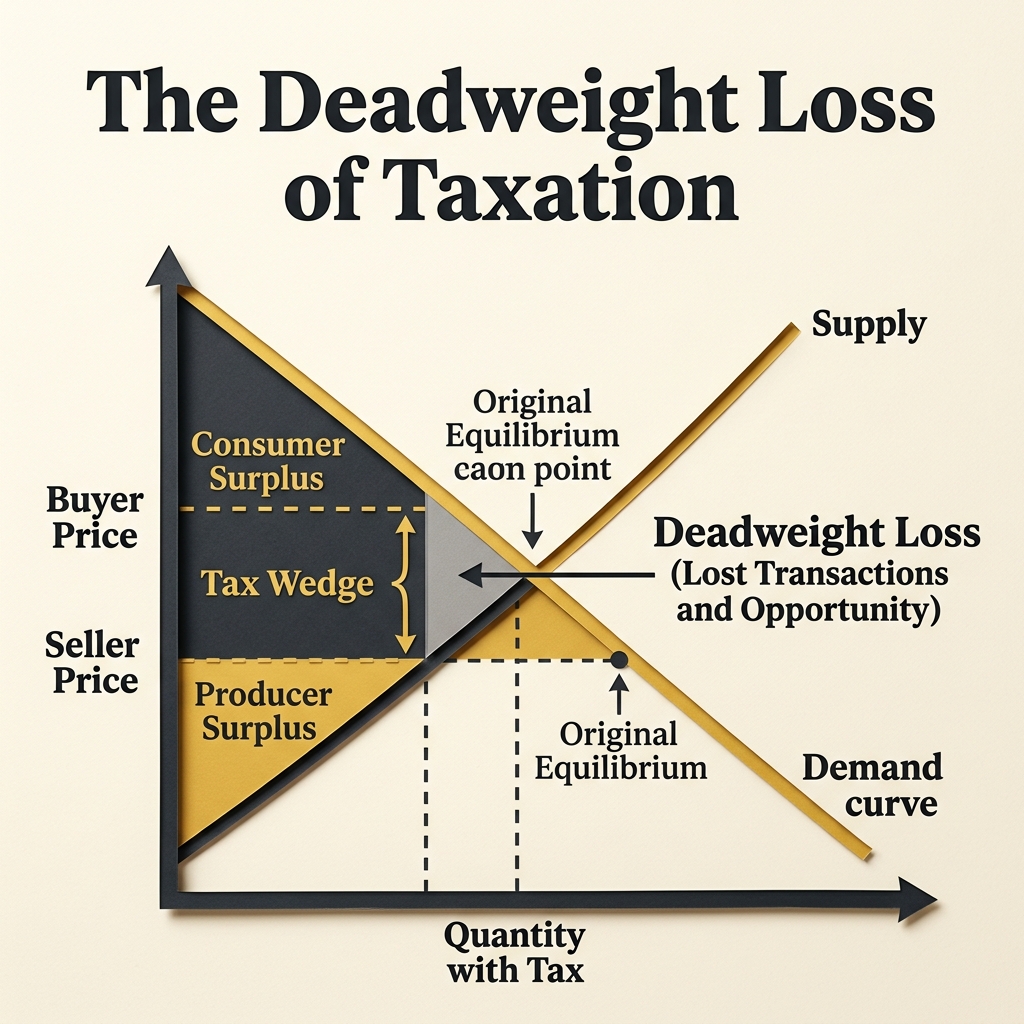

In the short run, taxation compresses corporate and individual profits, reducing the immediate pool of internal capital available for reinvestment. Taxes on capital gains, dividends, and corporate profits are direct levies on the reward for deferring consumption and taking investment risks.

When a tax is imposed on capital transactions, it creates a deadweight loss: a destruction of economic surplus that benefits neither the taxpayer nor the state. By raising the cost of transactions, taxes prevent mutually beneficial trades from occurring. For instance, high capital gains taxes create a lock-in effect, where investors choose to hold onto sub-optimal assets rather than selling them to invest in more productive ventures, simply to avoid triggering the tax liability. This transaction cost reduces the liquidity of capital markets, slowing down the reallocation of capital to high-value uses.

Long-Run Effects: Savings Depletion and Incidence Shifting

In the long run, the cumulative effect of taxation is the depletion of the society's total stock of capital. This depletion occurs because taxes are disproportionately drawn from funds that would have been saved rather than consumed. Low-income and middle-income individuals spend the majority of their income on consumption, while high-income individuals and corporations save and invest a significant portion of their earnings. By targeting corporate profits and high-income capital accumulation, the state extracts resources directly from the economy's investment engine.

This depletion is described by the Laffer Curve, formulated by the economist Arthur Laffer. The curve demonstrates that as tax rates rise beyond a certain threshold, the incentive to produce, save, and invest declines so significantly that the total tax base shrinks, leading to a reduction in total tax revenues for the state. By taxing capital gains and corporate profits, the state discourages the very activities that expand the tax base. This dynamic is exacerbated by double taxation; corporate earnings are taxed first at the corporate level, and then again when distributed to shareholders as dividends or realized as capital gains.

Furthermore, monetary inflation works as a stealth capital gains tax. Because capital gains taxes are calculated using nominal values rather than real purchasing power, price inflation subjects investors to taxes on losses. For example, if an investor purchases an equity asset for 100 dollars and sells it ten years later for 150 dollars, the tax authority registers a 50 dollar gain. However, if price inflation has reduced the value of the dollar by half during those ten years, the investor's real purchasing power has declined. The investor has experienced a real loss, yet the state imposes a capital gains tax on the nominal gain, directly confiscating private capital.

A smaller pool of savings leads to a higher cost of capital and lower levels of capital investment. Because the marginal productivity of labor: and therefore real wages: depends entirely on the quantity and quality of capital tools available to workers, the depletion of capital accumulation directly suppresses wage growth.

This demonstrates the economic reality of tax incidence: the legal entity that pays the tax to the government is rarely the entity that bears the economic burden of the tax. The corporate income tax provides a clear example. Corporations are legal fictions; they cannot bear taxes. The tax must be paid by real people. Economists observe that the burden of the corporate income tax is shifted in three directions:

- Labor: Shipped in the form of lower wages and reduced hiring, as the tax reduces corporate investment, lowering the marginal productivity of workers.

- Consumers: Shipped in the form of higher prices for goods and services, as firms treat the tax as an input cost that must be recovered through retail pricing.

- Shareholders: Shipped in the form of lower returns on equity, which reduces the value of pension funds, retirement accounts, and savings vehicles held by millions of ordinary citizens.

Furthermore, high taxation induces capital flight. In a globalized economy, capital flows to jurisdictions that offer the highest risk-adjusted returns and the most stable legal protections. When a state imposes confiscatory taxes on wealth or corporate profits, capital moves to low-tax nations. This migration deprives the domestic economy of the investment capital needed to maintain local industries, leading to deindustrialization and stagnant productivity.

Another critical distortion is the estate tax, often described as a wealth or inheritance tax. The estate tax represents a direct levy on accumulated family capital. When a capital owner dies, the state requires the heirs to pay a significant percentage of the asset value in cash. Because family businesses, farms, and manufacturing plants are often illiquid (with their value tied up in land, buildings, and machinery), heirs are frequently forced to liquidate these productive capital assets simply to pay the tax. This liquidation breaks up established capital units, destroys local jobs, and transfers wealth from productive, local enterprises to the state's consumptive budget, reducing the economy's long-run capacity to produce.

Regulation: The Calcification of Capital Allocation

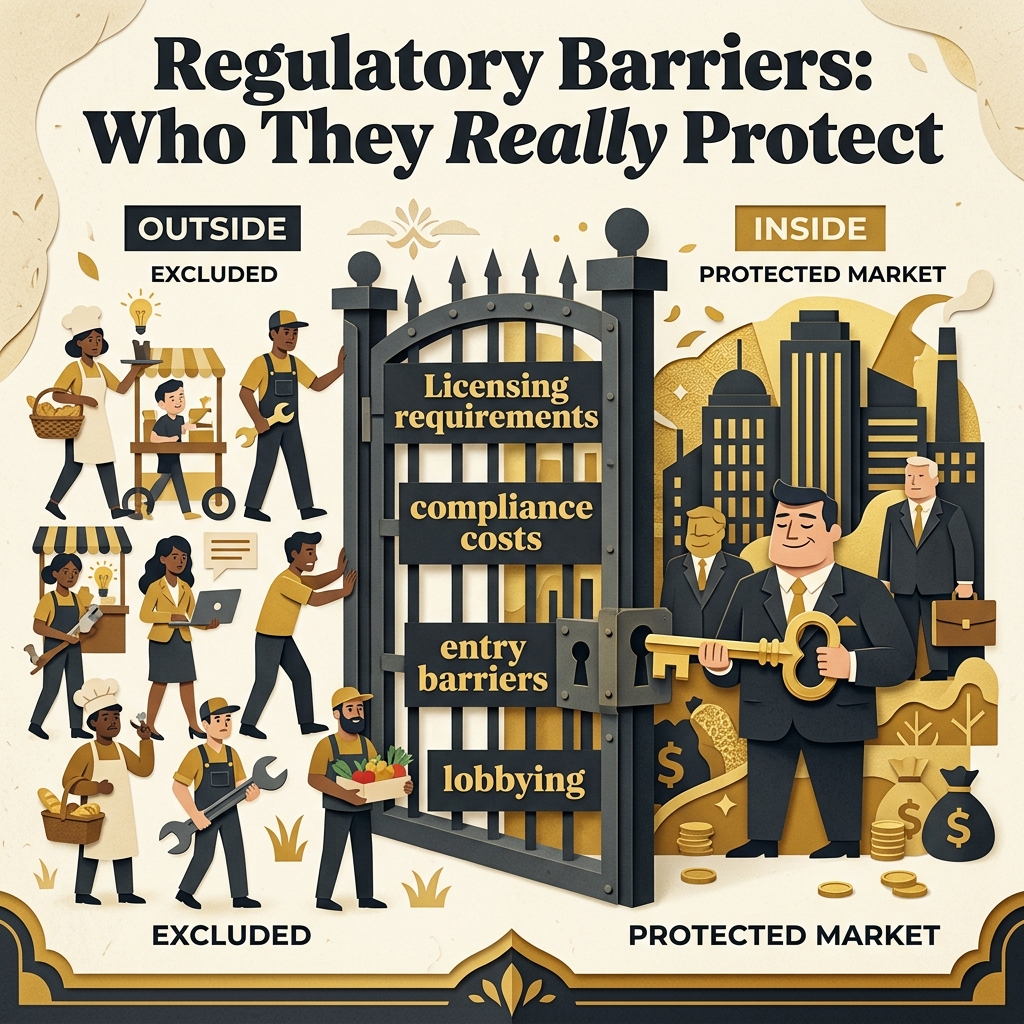

While inflation distorts capital prices and taxation extracts capital volume, regulation alters the path of capital allocation. Regulations are administrative directives issued by state bureaucracies that restrict how private actors can buy, sell, organize, or invest. Although these regulations are usually justified as protections against market failures, they act as state-enforced barriers to entry that calcify the existing economic structure.

Short-Run Effects: Compliance Costs and Resource Diversion

In the short run, regulation imposes significant compliance costs on firms. These costs include hiring compliance officers, lawyers, and lobbyists, purchasing specialized monitoring equipment, and navigating administrative delays. These expenditures do not add any value to the firm's final product; they are purely defensive costs incurred to avoid regulatory penalties.

For a business, compliance costs function as a tax on innovation. Capital that would have been spent on research and development, upgrading machinery, or expanding production capacity is instead diverted to regulatory administrative overhead. For early-stage firms and start-ups, these compliance costs can be ruinous, preventing them from achieving the scale necessary to compete with established competitors.

Long-Run Effects: Regulatory Capture and Cartelization

In the long run, regulation leads to regulatory capture and the cartelization of key industries. Regulatory capture occurs when the agencies created to regulate an industry become dominated by the largest firms in that industry. These large firms use the regulatory process to write rules that protect themselves from competition.

Large, established corporations have a significant advantage in navigating regulations. They can spread their compliance costs across a massive volume of output, reducing the cost per unit. For example, a multi-national bank can easily absorb the cost of compliance with thousands of pages of financial regulations, whereas a small community bank will find the compliance overhead unsustainable, forcing it to close or merge.

This regulatory asymmetry has been severely exacerbated by comprehensive financial regulations such as the Sarbanes-Oxley Act of 2002 and the Dodd-Frank Act of 2010. These laws imposed massive, fixed reporting and auditing requirements on publicly traded corporations. The high cost of compliance has driven a structural shift in capital markets. The number of publicly traded companies in the United States has declined significantly over the last two decades. Young, innovative firms choose to remain private much longer, or sell out to larger conglomerates, rather than incurring the expense of an Initial Public Offering (IPO).

Consequently, early-stage capital appreciation has shifted from public stock markets to private equity and venture capital funds. Because the state restricts access to private equity through accredited investor regulations, which require individuals to meet high income or net worth thresholds to invest, the high returns of early-stage growth capital are legally reserved for wealthy institutions and individuals. Retail investors are restricted to buying mature, low-growth public equities, widening the wealth gap.

By raising the minimum scale required to operate, regulations protect incumbent firms from the creative destruction of new competitors. This protection reduces the incentive for large firms to innovate, invest in new capital assets, or improve customer service. Capital markets, seeing that incumbent firms are protected by a regulatory shield, continue to fund these inefficient giants, while starving innovative start-ups of the capital they need to grow. The capital allocation process becomes politicized, directed toward compliance and lobbying rather than consumer satisfaction.

This regulatory calcification prevents the price mechanism from clearing bad investments. In a free market, businesses that fail to satisfy consumers or manage their resources efficiently are liquidated, and their capital assets are purchased by more capable entrepreneurs. Regulations and state bailouts interrupt this process, keeping zombie corporations alive on a diet of cheap credit and state protection. These zombie firms tie up labor and capital that could be used to build new, productive industries, depressing the economy's long-run growth rate.

A prime example of this regulatory calcification is the Certificate of Need (CON) laws that govern industries like healthcare. Under these statutes, an entrepreneur cannot build a new hospital, purchase advanced diagnostic machinery, or open a medical clinic unless they first prove to a state board that a "need" exists for the new facility. These boards are typically dominated by representatives from existing, incumbent healthcare providers who use the hearing process to block any new competitor. Consequently, capital that is eager to enter the healthcare market to build new clinics and lower consumer costs is legally turned away, protecting the monopoly profits of incumbent cartels and reducing the quality and availability of care for patients.

Short-Run Illusions vs. Long-Run Realities: The Broken Window

The common thread running through monetary inflation, taxation, and regulation is the prioritization of short-run political goals over long-run economic survival. This dynamic was famously analyzed by the French economist Frédéric Bastiat in his essay on the Seen and the Unseen: the fallacy of the broken window.

The short-run effects of government intervention are easily seen. The cheap credit boom creates visible construction sites, rising stock portfolios, and low nominal interest rates. The tax-funded government program creates visible infrastructure projects and public sector employment. The protective regulation offers visible safety standards or safeguards for domestic manufacturers.

The long-run structural decay, however, is unseen. The credit boom eventually collapses, leaving empty office towers, high debt loads, and a depleted savings pool. The tax-funded infrastructure project is paid for by the unseen private businesses that were never started, the upgrades to private machinery that were never purchased, and the real wage increases that workers never received because private capital was extracted. The regulation protects domestic manufacturers, but at the unseen cost of making consumers pay higher prices and preventing new, more efficient competitors from entering the market.

When the state attempts to stimulate the economy through monetary and fiscal expansion, it is not creating wealth; it is consuming its seed corn. A society that chooses to consume its capital base to fund short-run consumption or support politically favored industries will eventually face structural stagnation: a condition characterized by high inflation, declining productivity, and stagnant real wages.

Conclusion: The Necessity of Capital Market Autonomy

The accumulation of capital is the foundation of economic progress. It is the only mechanism by which human society can escape poverty and raise the standard of living for all citizens. A society with a large stock of capital tools can produce more goods per hour of labor, making products more affordable and work less physically demanding.

To accumulate and allocate this capital efficiently, capital markets must remain autonomous. They require a stable medium of exchange that cannot be inflated by central banks, a tax regime that does not penalize savings and risk-taking, and a regulatory environment that permits free competition and creative destruction.

When the state intervenes in these markets through inflation, taxation, and regulation, it disrupts the price signals that coordinate human action across time. The short-run gains of intervention are temporary illusions that are paid for by long-run structural decay. To secure sustainable prosperity, we must dismantle the regulatory and monetary monopolies of the state, allowing capital markets to return to their proper function: the peaceful, voluntary, and efficient coordination of human savings and investment for the future.