The debate over economic inequality is one of the most prominent of our time. From television screens to academic halls, we are presented with statistics showing that the wealth gap is widening, that a small percentage of the population controls a massive share of national assets, and that social mobility has stalled. The standard diagnosis from progressive commentators is that this disparity is a natural result of unregulated capitalism. The standard prescription is more state intervention: higher taxes on the wealthy, expanded social welfare programs, and more intensive regulation of business.

This diagnosis misses the true source of the problem. Economic inequality is not the natural outcome of free markets. It is the predictable consequence of state intervention. By implementing complex regulatory structures, inflating the money supply, taxing labor while protecting capital structures, and bailing out failing corporate giants, the government systematically creates an opportunity gap. It erects a wall of compliance around established industries, protecting the wealthy from competition while criminalizing the low-capital entrepreneurship that has historically allowed the poor to build wealth from scratch.

The Regulatory Fortress: Protecting the Incumbents

In a free market, wealth is temporary. A company can only remain wealthy by continually satisfying consumers better than its competitors. If a large corporation becomes lazy, charges high prices, or fails to innovate, it invites competitors. Entrepreneurs see the high profits, start competing firms, and bid away the incumbent's market share. This process of creative destruction is the natural check on concentrated economic power.

To stop this process, established businesses look to the state. Under the guise of public safety, environmental protection, or worker rights, they lobby for regulations. Public choice theory shows that regulations are frequently written by the very industries they are meant to regulate, a process known as regulatory capture.

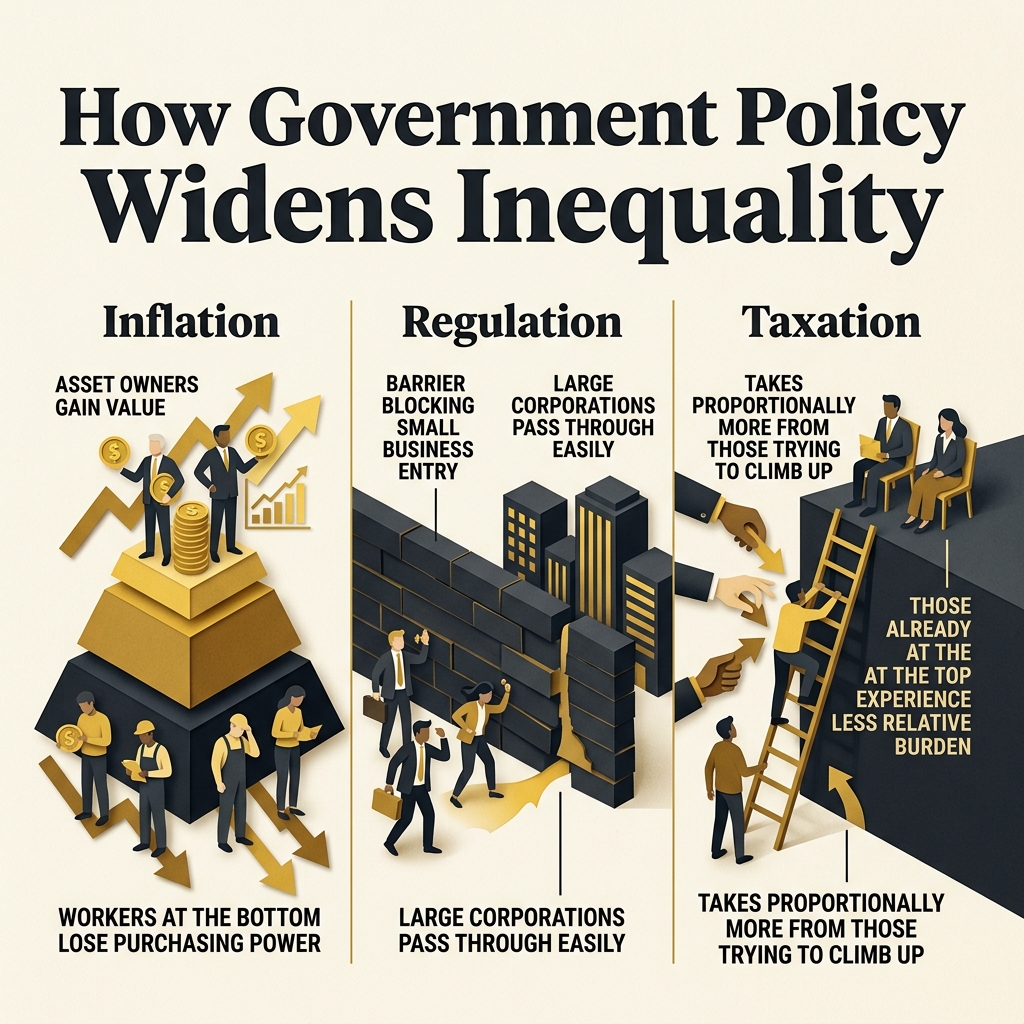

These regulations act as a fortress wall. A large, established corporation can easily absorb the cost of hiring a compliance department, maintaining teams of lawyers, and submitting detailed audits. For a small, under-capitalized competitor, these compliance costs are insurmountable. A regulation that costs one million dollars to comply with is a minor nuisance to a billion-dollar incumbent, but it is fatal to a startup. By raising the cost of starting a business, the regulatory state protects the wealth of incumbents from the competitive pressures of new entrants, locking out poor and middle-class entrepreneurs who cannot afford the entry fee.

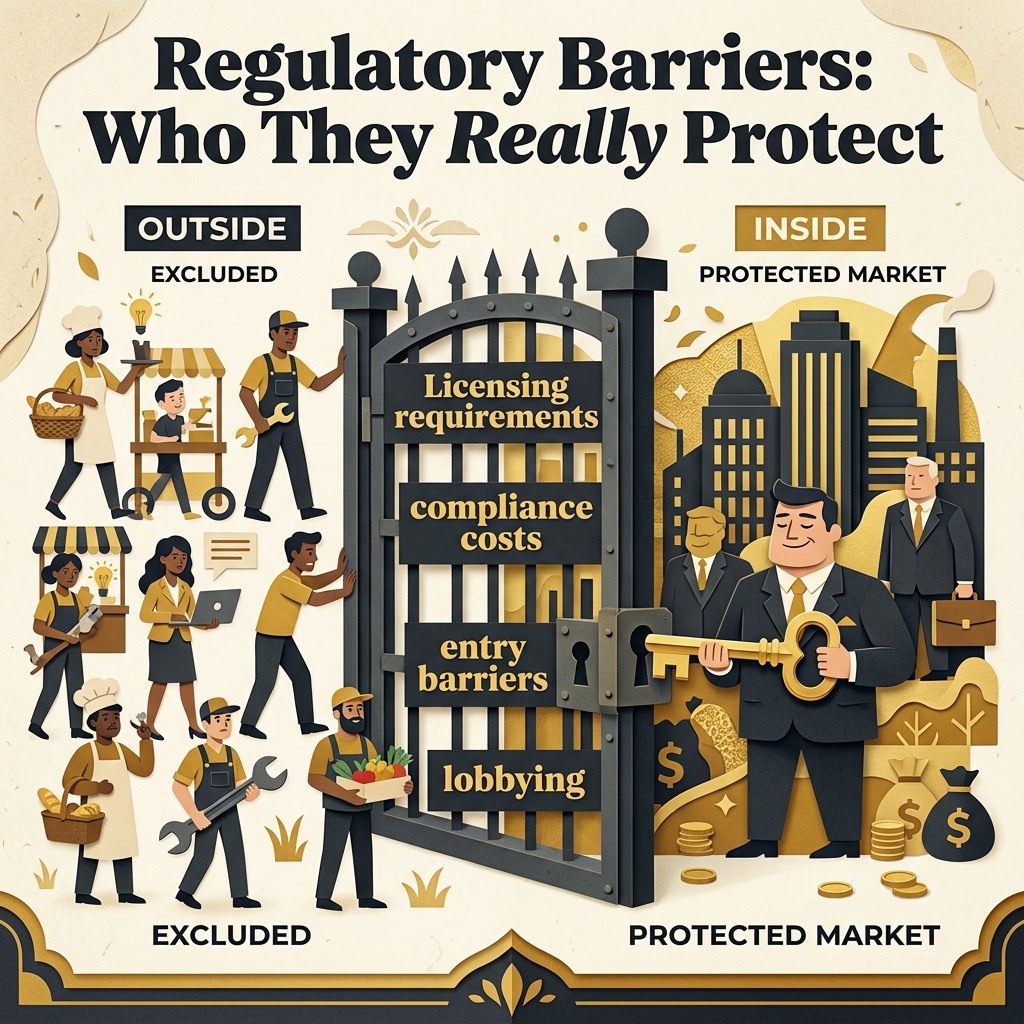

Occupational Licensing: Criminalizing the First Rungs

The most direct assault on the upward mobility of the poor is occupational licensing. In many parts of the world, it is illegal to sell one's labor without government permission. Licensing requirements have expanded from doctors and lawyers to include barbers, hair braiders, taxi drivers, florists, interior designers, and street vendors.

To obtain a license, a worker must pay hundreds of dollars in fees, undergo hundreds of hours of mandated training (often unrelated to safety), and pass exams. These barriers do not protect consumers; they protect existing practitioners from competition.

For a wealthy person, these fees and training hours are minor inconveniences. For a poor person who possesses a valuable skill (such as hair styling, cooking, or driving) but has no capital, these requirements make it illegal to work. If they attempt to offer their services without a license, they face fines or arrest. Occupational licensing criminalizes low-capital entrepreneurship, pulling the ladder of opportunity away from those who need it most, while keeping prices high for consumers.

The Inflation Gap: Cantillon Effects and Asset Disparity

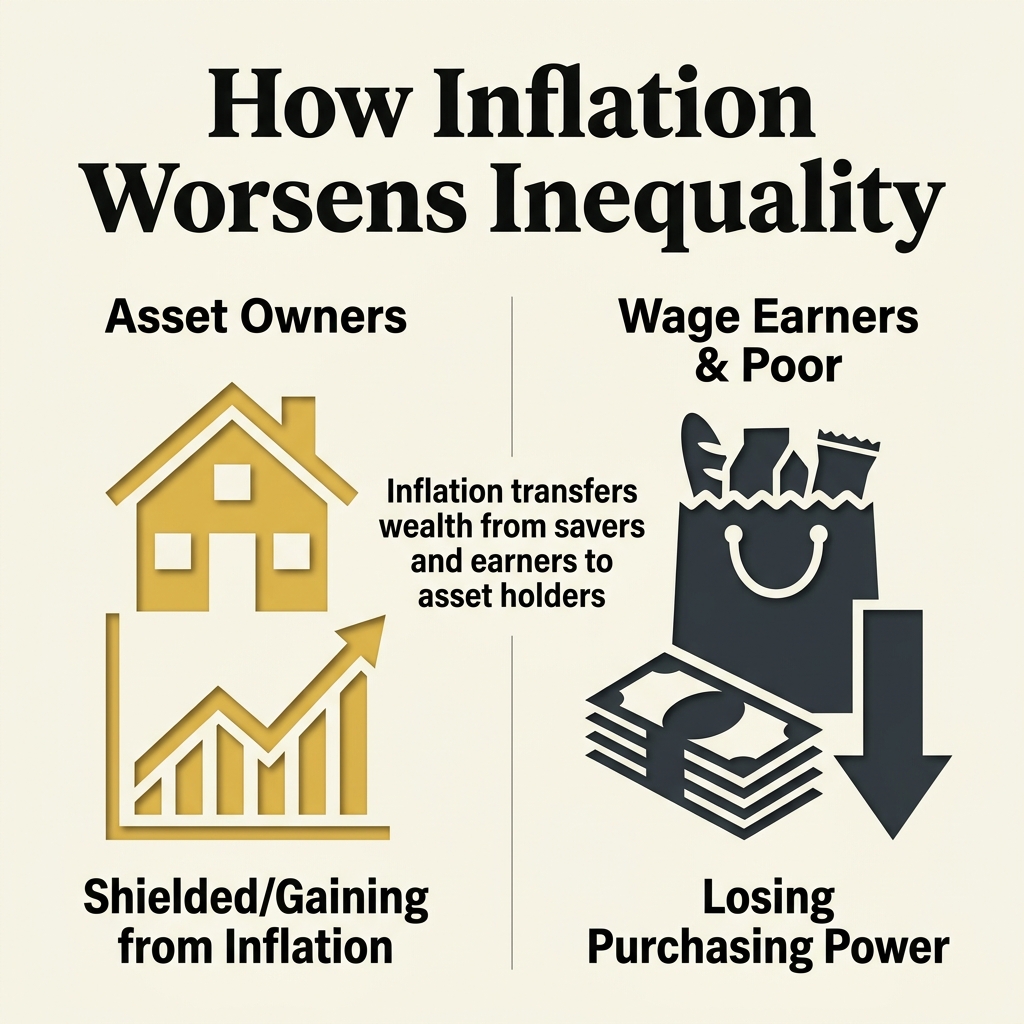

Central bank monetary expansion is a massive engine of inequality. When the Federal Reserve expands the money supply and lowers interest rates, it does not distribute the new money evenly. The money enters the economy through the banking sector.

The wealthy have access to this cheap credit first. They borrow money at artificially low rates to purchase assets like real estate, corporate stocks, and commodities. This massive influx of credit bids up the prices of these assets, creating a wealth boom for the asset-owning class.

The working class, who do not own portfolios of stocks or real estate, do not benefit from this asset boom. Their primary asset is their labor, and wages adjust slowly. As the printed money spreads through the economy, it bids up the cost of basic consumer goods: rent, groceries, healthcare, and energy. The working class pays higher prices for necessities, while their real wages are diluted. Inflation systematically transfers purchasing power from wage earners and cash savers to asset owners, widening the wealth gap through central bank policy.

Socialized Losses: The Corporate Bailout Culture

In a genuine free market, risk and reward are tied together. If an entrepreneur takes a risk and succeeds, they earn a profit. If they fail, they bear the loss. This discipline of profit and loss forces capital owners to invest responsibly.

In the modern corporatist economy, this link has been severed for the wealthy. Through the doctrine of too big to fail, governments bail out large banks, auto manufacturers, and financial institutions that have made bad investments.

When these companies succeed, their executives and shareholders capture the rewards. When they fail, the government steps in with taxpayer-funded loans, asset purchases, and subsidies. The losses are socialized, paid for by the working class through higher taxes and monetary inflation, while the rewards remain private. This moral hazard ensures that the wealthy are shielded from the consequences of their mistakes, preventing the natural redistribution of capital that occurs when failed businesses go bankrupt and their assets are sold to more capable operators.

Conclusion: The Path to Equal Opportunity

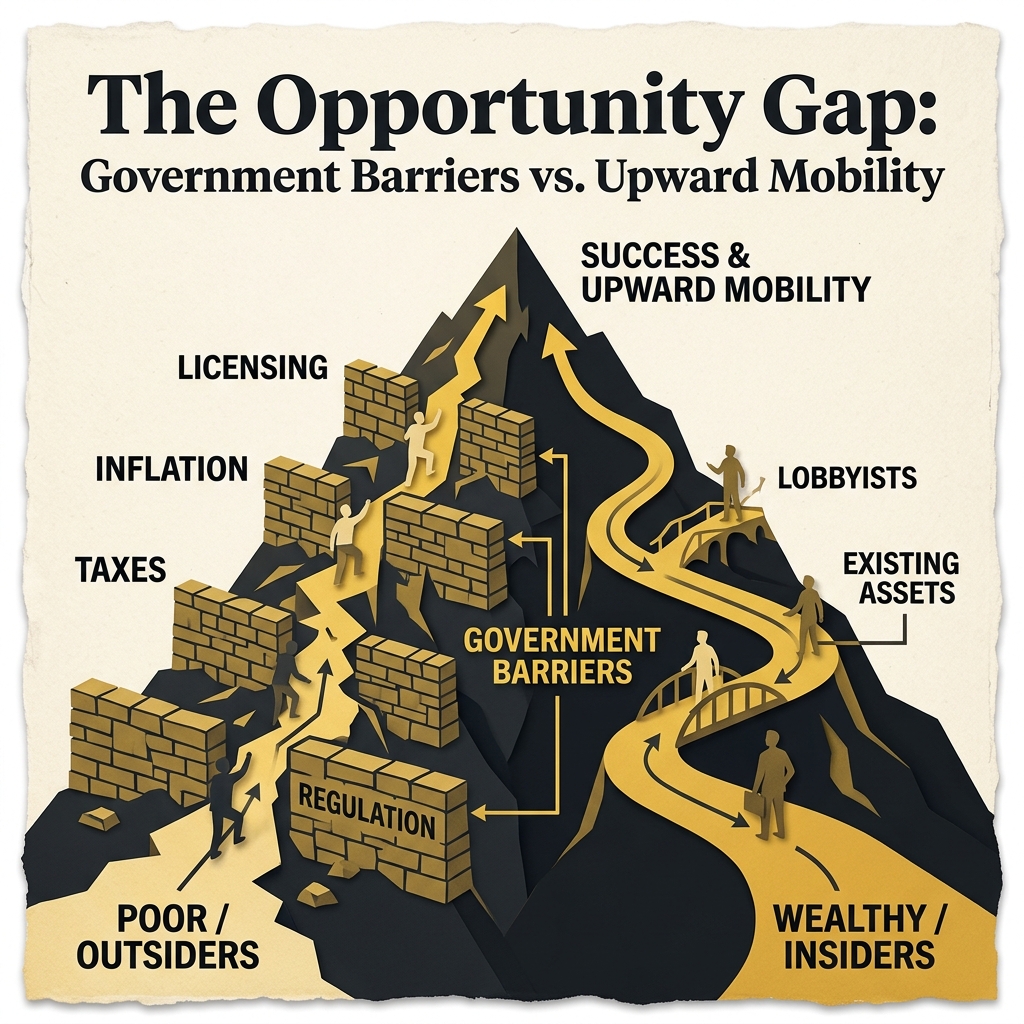

The widening wealth gap is a visible symptom of a deep structural disease. But that disease is not the free market. It is the systematic perversion of the market by government intervention.

When we tax the sale of labor while protecting existing assets, we stymie upward mobility. When we inflate the currency to fund government debt and bail out banks, we dilute the savings of the poor while inflating the assets of the rich. When we implement licensing laws and compliance regulations, we criminalize low-capital entry and protect corporate giants from the competition of the working class.

The solution is not to expand the state to tax and redistribute wealth, which only expands the bureaucracy and creates new opportunities for regulatory capture. The solution is to dismantle the regulatory fortresses, end the central bank credit expansions, abolish occupational licensing laws, and establish a genuine free market. Only when the market is free from state intervention can we have a system where upward mobility is based on productivity, work, and voluntary service to others, rather than political connections and lobbying power.