In modern political discourse, inflation is frequently treated as if it were a natural disaster. Media reports speak of inflation striking the economy or describe it as a mysterious consequence of supply chain disruptions, corporate greed, or geopolitical unrest. Central bankers promise to fight inflation using interest rate adjustments, portraying themselves as protectors of the currency's stability.

This narrative gets the relationship backwards. Inflation is not a random act of nature. In the classical and libertarian tradition, inflation is defined not as rising prices, but as the expansion of the money supply itself. Rising prices are merely the symptom. The source of inflation is the government and its central bank, which create money and credit out of thin air. This process does not create new wealth; it dilutes the value of existing currency, systematically transferring wealth from savers and wage earners to the state and financial elites, while trapping those at the bottom of the economic ladder.

The Source of Inflation: Monetary Expansion

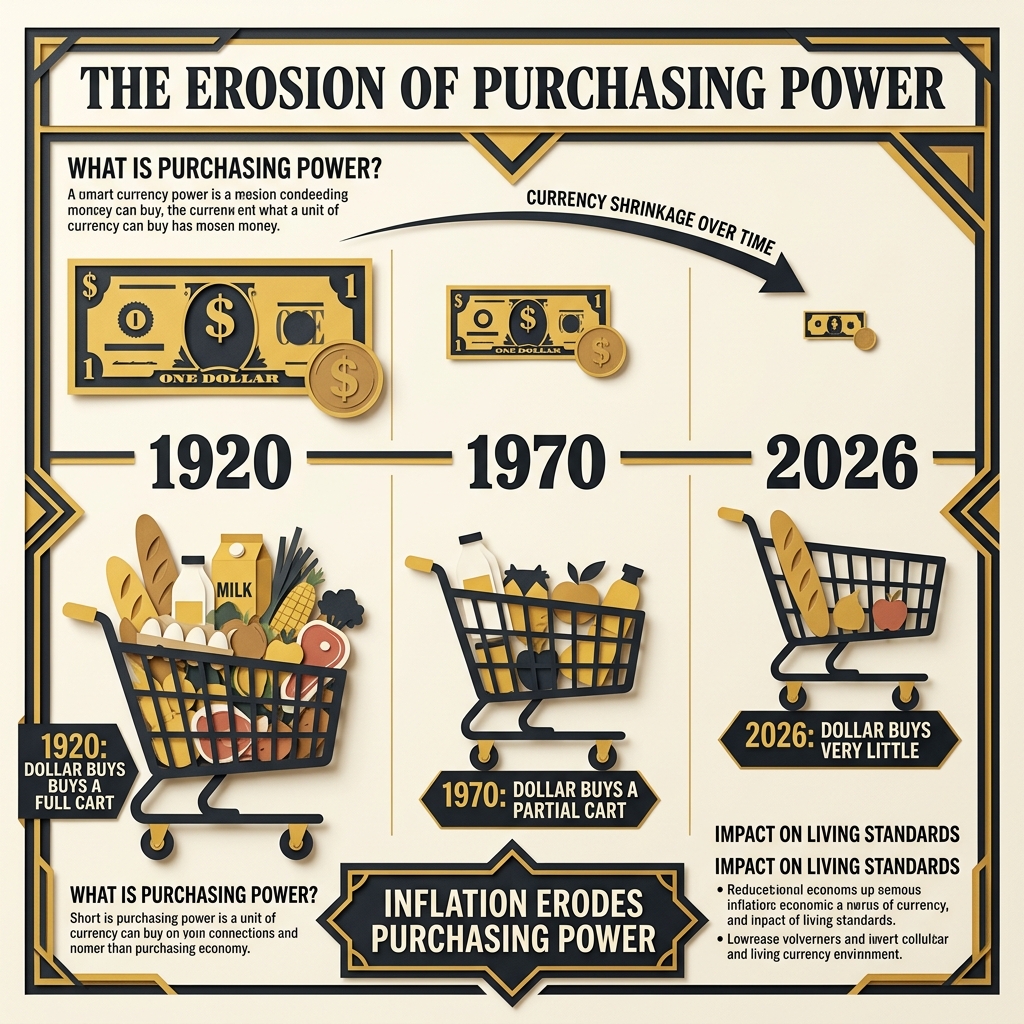

A market economy requires money to act as a medium of exchange, a unit of account, and a store of value. When the supply of goods and services grows, and the money supply remains stable, the purchasing power of money naturally rises. Prices fall. This is deflation, and in a free market, it is a sign of progress. It means that technological advancement and capital investment have made it cheaper to produce things, allowing workers to buy more with their wages.

Under a fiat monetary system managed by a central bank (such as the Federal Reserve), this process is reversed. Central banks target a positive rate of inflation (typically two percent), which means they commit to eroding the value of the currency by two percent every year.

To achieve this, the central bank continuously expands the money supply. It does this by buying government bonds, printing paper currency, and expanding the reserves of commercial banks, which then create new money through fractional reserve lending. When the quantity of money increases faster than the supply of actual goods and services, the value of each individual unit of money must fall. It requires more dollars to purchase the same amount of food, housing, energy, or stocks.

The Mechanics of Money Production

To understand how inflation is produced, one must look at the mechanics of the modern banking system. In a fiat system, money is not backed by a physical commodity like gold. Instead, it is created as debt.

The process begins when the Federal Reserve conducts open market operations. When the central bank wants to expand the money supply, it purchases US Treasury bonds from private banks. The Fed does not pay for these bonds with existing funds; it simply writes check-like credits to the banks' reserve accounts at the Fed. The central bank creates new reserves with a keystroke.

Once the commercial banks have these new reserves, they do not hold them in vault cash. Under the fractional reserve banking system, banks are permitted to lend out a multiple of their reserves. If the reserve requirement is ten percent, a bank can lend out ninety dollars for every ten dollars it holds in reserve. When a bank grants a loan, it does not hand over cash; it creates a new deposit account for the borrower. The bank creates new checkbook money out of nothing. As these loans are spent and deposited in other banks, the process repeats, multiplying the initial injection of Fed reserves into a much larger volume of broad money.

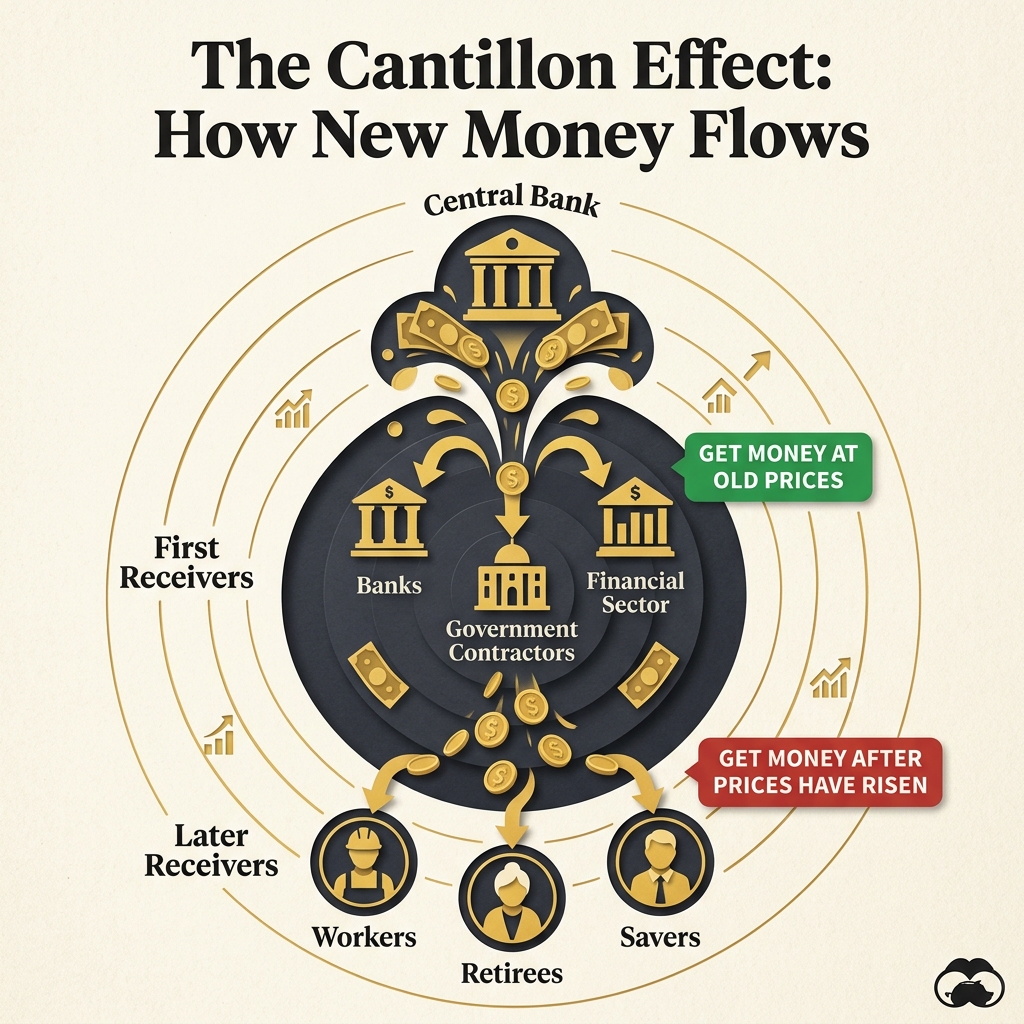

The Cantillon Effect: The Silent Redistribution

If newly printed money were distributed instantly and evenly to every citizen, inflation would be relatively harmless. Everyone's nominal cash holdings and income would double, and all prices would double, leaving real wealth unchanged.

In the real world, money creation does not work this way. Newly created money enters the economy at specific points. The first recipient is the government itself, followed by commercial banks, primary dealers, and large, government-favored corporations. This unequal distribution of new money creates a phenomenon first described by the eighteenth-century economist Richard Cantillon, known as the Cantillon effect.

The early recipients of the new money spend it before prices have risen. They purchase real estate, raw materials, and corporate assets at the old, lower prices. As this new money is spent, it cascades through the economy, bidding up prices.

By the time the new money reaches the late recipients (wage earners, pensioners, and the poor who live far from the financial centers), the prices of consumer goods have already risen. Their incomes have not changed, but their cost of living has soared. The Cantillon effect is a silent, regressive transfer of purchasing power from savers and low-income earners to the state, commercial banks, and the asset-owning classes.

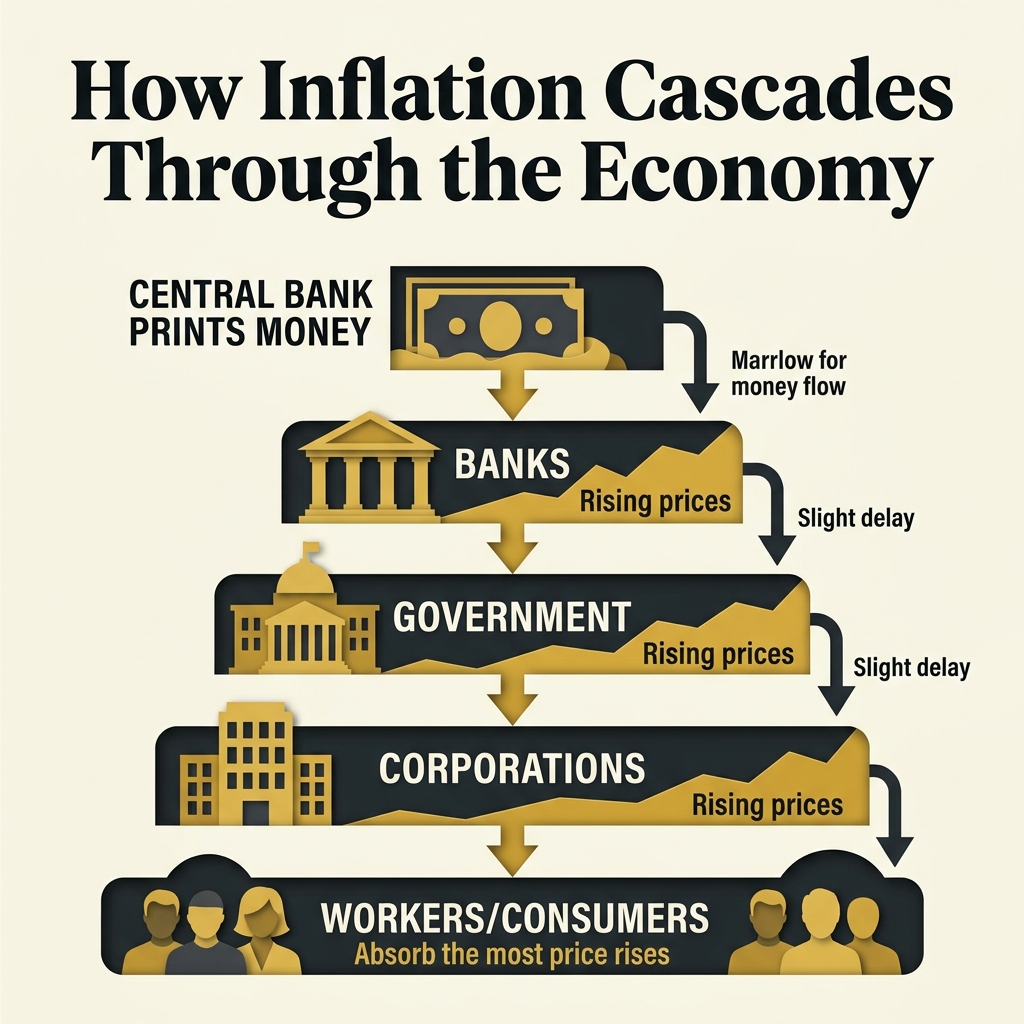

This cascade pattern explains why asset price inflation typically precedes consumer price inflation. When the Federal Reserve lowers interest rates and injects new reserves into the banking system, that money does not flow immediately into the grocery store. It flows into Wall Street.

Investment banks and hedge funds use the cheap credit to bid up the prices of equities, bonds, and luxury real estate. This creates a wealth effect for the asset-owning class, whose portfolios rise in value. By the time this wealth is spent on real-world goods and services, it drives up the prices of oil, food, and rent. The wealthy benefit from the asset bubble, while the working class suffers from the resulting increase in the cost of living.

The Relationship of Inflation to Government Deficits

Mainstream commentators often treat monetary policy and fiscal policy as separate domains. In reality, the central bank and the government treasury operate as a unified fiscal system, and inflation is the primary mechanism by which the state finances its deficits.

When a government spends more than it collects in taxes, it runs a deficit. To cover this deficit, the Treasury must borrow money by issuing government bonds. In a sound monetary system, these bonds are purchased by private savers who defer their own consumption. The total amount of money in the economy remains constant; purchasing power is simply transferred from private savers to the state.

However, modern democratic governments run deficits that are far larger than the pool of private savings can support. If the Treasury attempted to fund these deficits solely through private borrowing, the demand for loans would exceed the supply of savings, driving interest rates up. High interest rates make government borrowing prohibitively expensive and crowd out private investment, leading to economic contraction.

To prevent this, the central bank steps in to monetize the debt. The Fed purchases government bonds directly or indirectly through primary dealers, paying for them with newly created reserves. This process (often described as quantitative easing) is monetary debasement.

The central bank prints the money that the government needs to cover its deficits. Inflation is not a random market failure; it is the inevitable consequence of a state that refuses to balance its budget. The government uses the inflation tax to fund its programs, wars, and welfare state without having to pass explicit, unpopular tax increases.

Theories of Interest Rates and Inflation

To understand the relationship between inflation and interest rates, one must examine the competing economic schools of thought that have attempted to analyze these phenomena.

1. Eugen von Böhm-Bawerk and Time-Preference Theory

In the Austrian tradition, interest is not the price of money; it is the price of time. Eugen von Böhm-Bawerk, in his landmark work Capital and Interest, established the time-preference theory of interest.

Böhm-Bawerk observed that human beings naturally value present goods more highly than future goods. A person prefers to have a house, a car, or a meal today rather than ten years from now. To induce a person to defer consumption and save their resources, they must be offered a premium: a reward in the future that is larger than the sacrifice made in the present.

This time-preference rate determines the natural rate of interest. If a society has a low time preference (meaning people are willing to save for the long term), savings will be high, and the interest rate will naturally fall. This low interest rate signals that capital is available for long-term, productive investments.

Conversely, if a society has a high time preference (people want to consume today and save little), savings will be low, and interest rates will rise, signaling that capital is scarce and long-term projects are not viable.

Böhm-Bawerk's theory was expanded by Ludwig von Mises and Friedrich Hayek to explain how artificial credit expansion distorts the "structure of production." In a healthy market, the length of productive processes (which Böhm-Bawerk called "roundaboutness") is constrained by real savings. When the central bank artificially suppresses interest rates, it fools entrepreneurs into believing that the pool of savings is larger than it actually is.

Entrepreneurs launch highly roundabout, long-term projects (like infrastructure, heavy industry, or real estate developments) that require more capital than is actually available. This leads to a systematic coordination failure. As these projects consume resources, the scarcity of real savings is exposed, the central bank is forced to stop printing money, interest rates rise back to their natural level, and these projects collapse. The boom-bust cycle is the direct result of the central bank separating the interest rate signal from the real savings rate.

2. Milton Friedman and the Quantity Theory of Money

In the Monetarist tradition, Milton Friedman revived the quantity theory of money, famously stating that "inflation is always and everywhere a monetary phenomenon."

Friedman utilized the equation of exchange: M times V equals P times Y, where M is the money supply, V is the velocity of money (how often a unit of currency is spent), P is the price level, and Y is real output.

Friedman argued that in the long run, velocity (V) and real output (Y) are determined by real factors (technology, demographics, and labor productivity) not by the money supply. Therefore, any sustained increase in the money supply (M) must lead directly to a proportional increase in the price level (P).

While the Austrian school focuses on the structural distortions caused by the path of new money (Cantillon effects), the Monetarist school focuses on the aggregate price level, arguing that stable monetary growth is the key to preventing economic cycles.

3. The Fisher Effect

Economist Irving Fisher established the relationship between inflation and nominal interest rates, known as the Fisher effect. Fisher showed that the nominal interest rate (the rate you see at the bank) is equal to the real interest rate plus the expected rate of inflation: Nominal Rate = Real Rate + Expected Inflation.

When the public expects high inflation, lenders demand higher nominal interest rates to protect their purchasing power, and borrowers are willing to pay them because they expect to pay back the loans with depreciated currency.

This creates a conflict for the central bank. If the Fed prints money to keep interest rates low, it eventually triggers price inflation. Once the public realizes that inflation is rising, they demand higher interest rates, forcing the Fed to choose between raising rates (which can trigger a recession) or printing even more money to suppress rates (which can trigger hyperinflation).

Effects on Capital Markets, Risk-Taking, and Asset Bubbles

When the central bank manipulates interest rates and inflates the money supply, it alters the structure of capital markets and changes the risk tolerance of investors.

The Search for Yield

In a sound monetary system, savers can preserve their wealth by holding cash or low-risk government bonds. These assets provide a modest return that matches the growth of the economy, allowing individuals to prepare for retirement without taking on significant risk.

When the central bank targets a positive inflation rate and suppresses nominal interest rates below the rate of inflation, savers face a negative real return. If inflation is five percent and a bank account pays one percent, the saver is losing four percent of their purchasing power every year.

This forces savers out of low-risk assets into risky capital markets in what is known as the "search for yield." Retirees, pension funds, and ordinary citizens are forced to invest in corporate equities, high-yield junk bonds, real estate, and speculative assets simply to preserve their purchasing power. This influx of capital drives up asset prices, creating speculative bubbles that are disconnected from economic reality.

Debt-Financed Speculation and Asset Volatility

This hunt for yield is accompanied by corporate capital restructuring. Under negative real interest rates, the cost of borrowing is lower than the rate of inflation, incentivizing corporations to load their balance sheets with debt.

Instead of using debt to invest in productive research or machinery, companies use the cheap credit to fund share buybacks. By reducing the number of outstanding shares, they artificially inflate their earnings-per-share metrics, triggering executive bonuses while leaving the company highly leveraged and fragile. The capital structure of the corporate sector becomes skewed toward debt over equity, increasing systemic bankruptcy risks when the monetary policy inevitably tightens.

Moral Hazard and the Greenspan Put

By suppressing interest rates and bailing out financial institutions during crises, the central bank creates a system-wide moral hazard. Investors and corporations realize that the state will protect them from the consequences of their risky behaviors.

This expectation of central bank support is often referred to as the "Greenspan Put" (or the Fed Put). When asset prices decline, the central bank responds by lowering interest rates and injecting liquidity, bailing out the leveraged speculators.

This encourages corporations to increase their leverage, borrow money to fund share buybacks, and reduce their cash reserves. The financial system becomes highly fragile, dependent on continuous injections of cheap credit to prevent a general collapse. The natural market mechanism of risk management is destroyed, replaced by a speculative casino where profits are privatized and losses are socialized.

Other Unintended Consequences of Monetary Intervention

Beyond price inflation and asset bubbles, central bank monetary intervention produces several long-term, structural distortions that erode the economy's productivity and moral foundations.

1. Capital Consumption

In a market economy, capital is the collection of tools, machinery, factories, and infrastructure that makes labor productive. To build capital, a society must save: it must produce more than it consumes, and invest the surplus in capital goods.

Inflation distorts this calculation, leading to capital consumption. When inflation is high, corporate profits are overstated because accounting rules do not fully account for the rising replacement cost of capital goods.

For example, if a machine costs $10,000 to purchase, and inflation drives the replacement cost to $20,000, a corporation that sets aside depreciation based on the historical cost will find itself unable to purchase a new machine when the old one wears out. The corporation has unknowingly consumed its capital, paying out phantom profits that were actually a return of capital, not a return on capital. Over time, this hollows out the industrial base, leaving the economy less productive and wages stagnant.

2. The Rise of Zombie Corporations

By keeping interest rates artificially low for extended periods, the central bank allows inefficient, unprofitable firms to survive. These are known as "zombie corporations": companies that do not earn enough profit to cover their debt service costs, and can only survive by continuously refinancing their debt with cheap credit.

In a free market, these failing firms would go bankrupt. Their assets (real estate, patents, machinery, employees) would be liquidated and purchased by more efficient, profitable companies. This process of creative destruction is essential for economic growth.

By preventing these bankruptcies, the central bank freezes capital in unproductive uses, stymieing productivity growth and locking workers into dead-end jobs at failing companies. The economy becomes clogged with debt-bloated conglomerates that drag down overall efficiency.

3. High Time Preference and Cultural Decay

Monetary debasement has a profound effect on a society's cultural values. When the value of money is stable, individuals are encouraged to save, plan for the future, and engage in long-term projects. They adopt a low time preference.

When the currency is constantly losing value, saving is penalized. The rational choice is to spend today before prices rise tomorrow. The society adopts a high time preference: a focus on short-term consumption, immediate gratification, and debt accumulation.

This shift from saving to consumption erodes the moral foundations of a free society. It encourages a culture of short-sightedness, where long-term planning (such as family formation, capital investment, and educational attainment) is replaced by speculative risk-taking and instant consumption. The state steps in to fill the void left by depleted family savings, expanding the welfare state and increasing dependency on the government.

Current Levels of Monetary Policy in the United States

To analyze the contemporary economy, one must look at the specific policies of the Federal Reserve and the structural constraints that limit its actions.

Interest Rate Targeting and Quantitative Easing

In the wake of the 2008 financial crisis and the 2020 pandemic response, the Federal Reserve adopted unprecedented policies. It lowered its target interest rate to near zero and launched massive bond-buying programs: quantitative easing (QE).

Between 2008 and 2022, the Federal Reserve's balance sheet expanded from less than one trillion dollars to nearly nine trillion dollars. This massive injection of reserves inflated the prices of assets (housing, equities, bonds, and venture capital) and eventually cascaded into consumer price inflation.

To fight the resulting consumer inflation, the Fed was forced to raise interest rates rapidly in 2022 and 2023, shifting from quantitative easing to quantitative tightening (QT), where it allowed government bonds to mature off its balance sheet without replacing them.

The Debt Service Trap

The Federal Reserve's attempt to normalize interest rates has run into a major fiscal barrier: the size of the US national debt, which exceeds $34 trillion.

When interest rates were near zero, the government could service its debt at a very low cost. As the Fed raises rates, the interest expense on the national debt rises rapidly. If interest rates remain at five percent, the annual interest payment on the national debt will soon exceed one trillion dollars, making interest payments the largest single item in the federal budget, surpassing defense and social welfare programs.

This creates a structural trap for the central bank. If the Fed keeps interest rates high to fight inflation, it will drive the government into fiscal bankruptcy, forcing the Treasury to borrow even more money simply to pay the interest on its existing debt.

If the Fed lowers interest rates to save the government from default, it must print money to buy the government's bonds, triggering another wave of monetary debasement and price inflation. The central bank has lost its independence, captured by the fiscal demands of the state.

Alternative Monetary Approaches

For libertarians, the solution to monetary instability is not to replace one Fed chairman with another or to write new regulations for the central bank. The solution is to abolish the state's monopoly on money and allow the market to discover the most stable medium of exchange.

1. Competing Currencies and Free Banking

The most natural market alternative is a system of competing currencies and free banking, a concept championed by Friedrich Hayek in his monograph The Denationalization of Money.

Under a free banking system, the state does not issue currency. Instead, private banks issue their own banknotes, which compete in the marketplace. These banknotes are backed by real assets (gold, silver, or baskets of commodities) and are redeemable on demand.

In a free banking framework, banks manage their notes through clearing houses. A clearing house is a private association of banks that settle balances between members. If a bank over-issues its notes, the clearing house will collect these notes and present them to the issuing bank for redemption in reserve assets. This daily clearing mechanism acts as an automatic brake on credit expansion.

If a bank prints too many notes and cannot fulfill its redemption obligations, it faces bankruptcy. This threat of bankruptcy forces banks to act prudently and maintain stable reserves, preventing the expansion of credit that drives the business cycle. The market regulates the money supply through the price mechanism and competition, ensuring stable prices and protecting the savings of the public.

2. The Gold Standard

A more traditional alternative is the classical gold standard, where the currency unit (the dollar) is defined as a specific weight of gold. The gold standard limits the money supply to the physical quantity of gold mined, preventing politicians from expanding the currency to cover deficits.

While the gold standard provided remarkable price stability during the nineteenth century, its primary weakness is its vulnerability to state capture. Throughout history, governments have suspended the gold standard during wars and crises to print money, eventually abandoning the system entirely in favor of fiat currency.

3. Decentralized Digital Assets

In the twenty-first century, decentralized digital assets like Bitcoin offer a technological alternative to central banking. Bitcoin's key feature is its fixed supply: only 21 million units will ever exist, written directly into the open-source software code.

Because Bitcoin is decentralized and operates on a peer-to-peer network, it cannot be manipulated by central banks or seized by governments. It represents a form of non-state money that operates outside the corporatist financial system, allowing individuals to save and trade without risk of debasement.

The Effects on Libertarian Ends

Ultimately, the critique of inflation is not merely technical or economic; it is moral. Monetary debasement directly undermines the libertarian ends of a free, prosperous, and peaceful society.

First, inflation violates property rights. When the state prints money, it dilutes the value of the dollars held by citizens, extracting their wealth without their consent. It is a form of state-sanctioned theft that is hidden behind economic complexity.

Second, inflation expands the scope of the state. By eroding the savings of the poor and middle class, inflation creates a class of dependent citizens who demand government support, price controls, and welfare programs to survive. This dependency is then used by politicians to justify new interventions, taxes, and regulatory agencies, leading to a gradual decline in individual liberty.

Third, inflation fosters social conflict. By redistributing wealth from labor to asset owners, inflation generates class resentment and polarization. The public blames the market, corporations, or foreign adversaries for the rising prices, unaware that the central bank is the source of their plight.

Only by restoring sound money can we protect individual property rights, restore social trust, and build a free society where upward mobility is a natural result of productive work and voluntary exchange.