For nearly a century, the debate over how to manage a modern economy has revolved around a central question: can a free market coordinate itself, or does it require the steadying hand of the state to prevent collapse? Neoclassical economics assumed that markets naturally tend toward full employment and equilibrium. The Great Depression of the 1930s shattered that confidence. In the midst of that crisis, a British economist named John Maynard Keynes proposed a radical new framework that changed the relationship between government and the economy forever.

The Keynesian School of Economics shifted the focus of economic analysis from individual markets and prices to aggregate demand: the total spending of an entire society. In the Keynesian view, recessions occur because of insufficient demand, and the only entity large enough to fill the gap is the state. While this approach dominated policy circles in the post-war era, libertarians and free-market economists have consistently pointed to its structural flaws, its inflationary bias, and its erosion of individual liberty.

The Great Disruption: The Crisis of Classical Orthodoxy

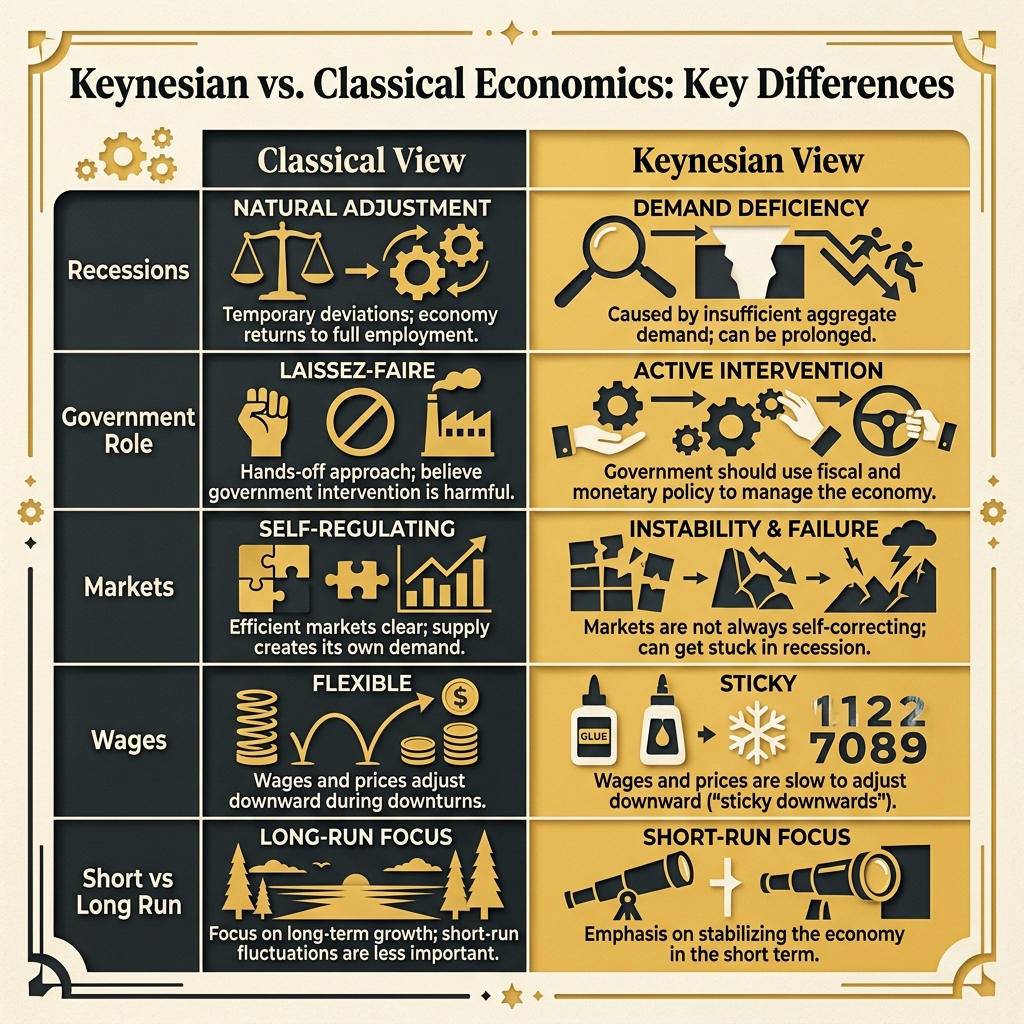

To understand the rise of Keynesianism, one must understand the intellectual environment of the early 1930s. Classical and neoclassical economic theory held that markets were self-correcting. According to Say's Law, named after the French economist Jean-Baptiste Say, supply creates its own demand. The act of producing goods generates income for workers and owners, which is then spent to purchase those goods. If a temporary surplus of goods or labor occurs, prices and wages will fall, inducing buyers to purchase more and employers to hire more, restoring full employment.

The Great Depression seemed to defy this logic. Year after year, unemployment remained high, factories sat idle, and investment languished. Wages and prices fell, but the correction did not arrive. Classicists argued that the depression was prolonged by government policies that kept wages artificially high and restricted trade. But to a desperate public and political class, the classical advice to wait for the market to self-correct was politically unacceptable.

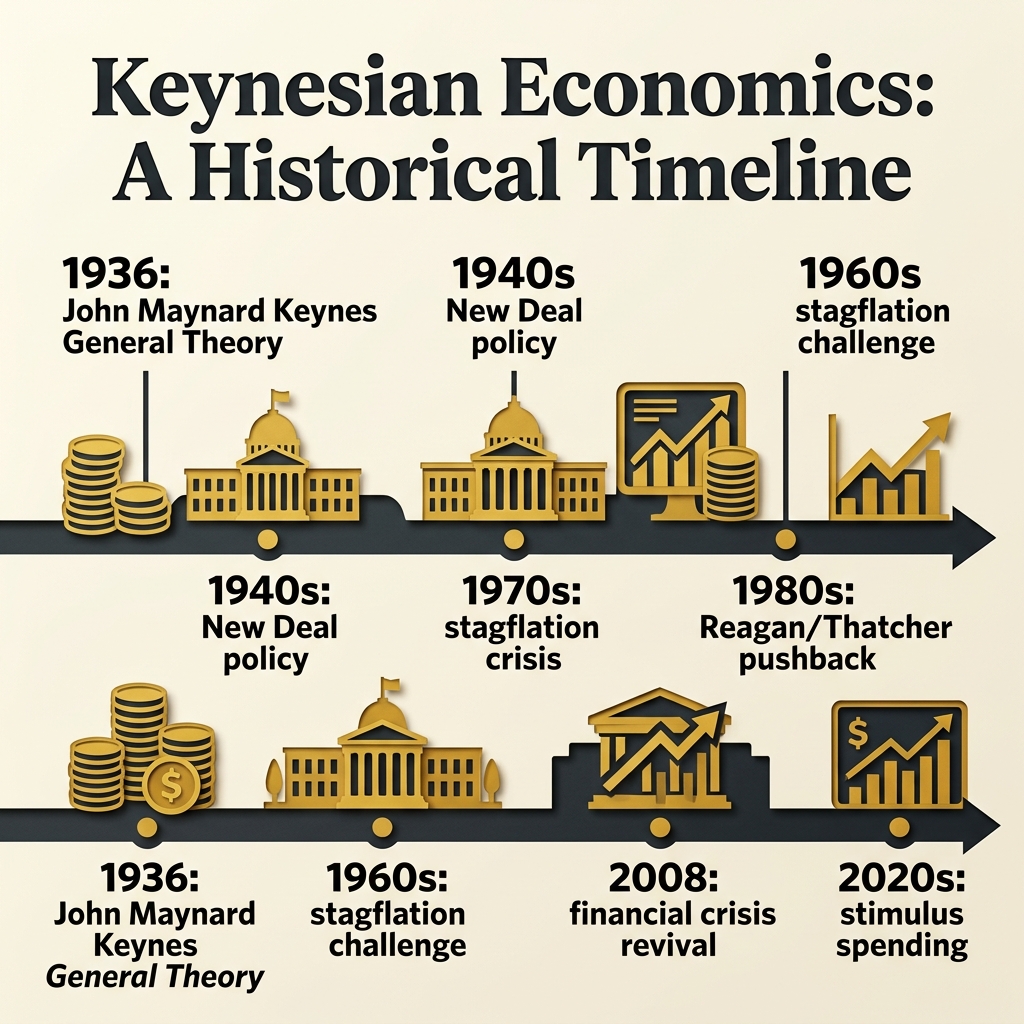

John Maynard Keynes (1883-1946) stepped into this void. In his 1936 book, The General Theory of Employment, Interest, and Money, Keynes launched a direct assault on the classical orthodoxy. He argued that a market economy could become stuck in an underemployment equilibrium, a stable state where resources remained idle and unemployment persisted indefinitely because of a lack of spending.

Aggregate Demand and the Mechanics of the General Theory

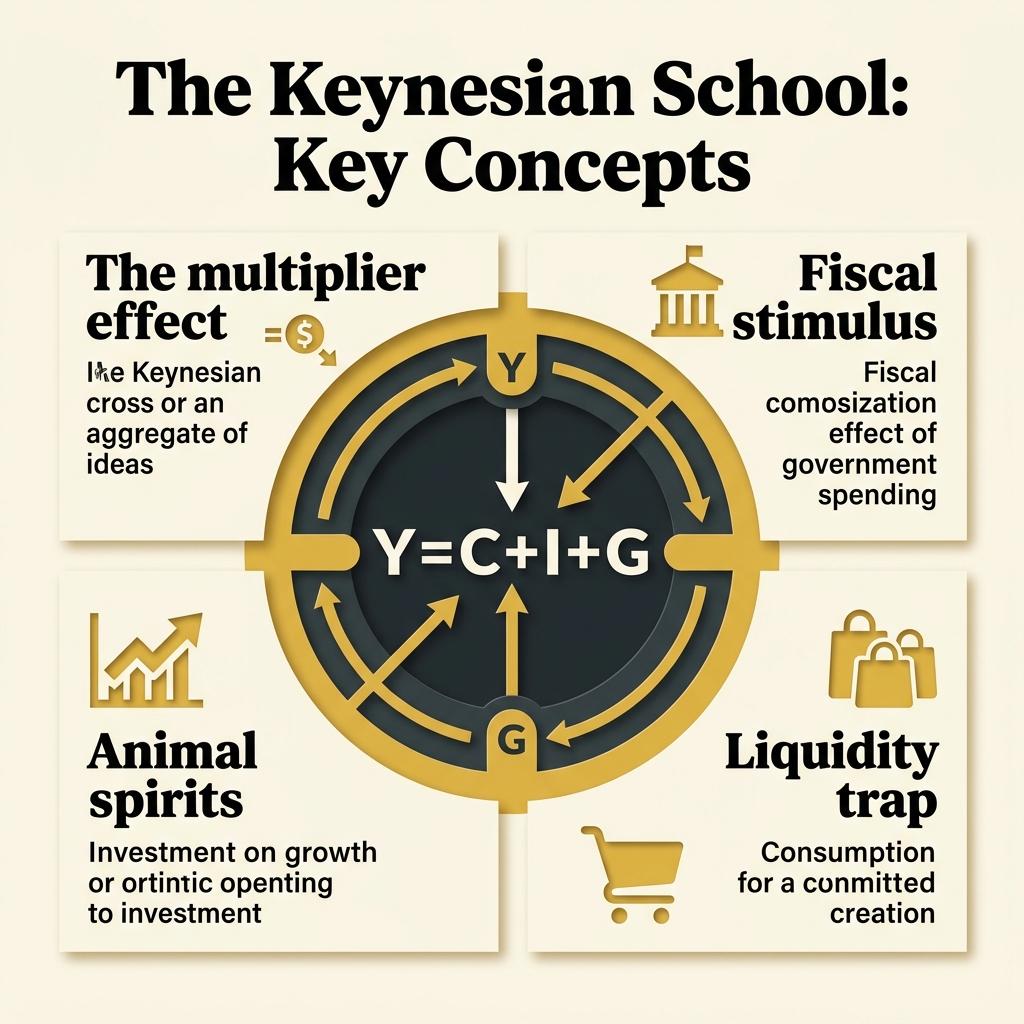

Keynesian theory is built on the concept of aggregate demand, which is the sum of consumption, investment, government spending, and net exports. In the classical view, savings are always converted into investment through adjustments in the interest rate. If savings increase, the supply of loanable funds rises, interest rates fall, and businesses borrow more to invest.

Keynes argued that this mechanism was broken. Savings and investment are decided by different people for different reasons. Savings depend largely on income levels, while investment depends on business expectations of future profitability. Keynes introduced the term animal spirits to describe the emotional, psychological, and non-rational factors that drive business investment decisions. When optimism is high, investment booms; when pessimism takes hold, investment collapses, regardless of low interest rates.

Furthermore, Keynes argued that wages and prices are sticky downward. Workers resist wage cuts, and contracts, labor unions, and social norms prevent wages from falling quickly during a downturn. Because wages do not adjust immediately, a fall in demand leads to layoffs rather than lower costs. As unemployment rises, worker income falls, leading to further declines in consumption spending. A downward spiral begins, pulling the economy deeper into depression.

Keynes also introduced the concept of the multiplier. The basic idea is that any initial change in spending has a magnified effect on total income. If the government spends money to build a road, the construction workers receive income, which they spend on food, clothing, and housing. The merchants who sell these goods receive income, which they spend in turn. In this way, an injection of spending cascades through the economy, generating total income greater than the original expenditure.

The Policy Prescription: Counter-Cyclical Fiscal Policy

The policy recommendations of the Keynesian School flow directly from its diagnosis of recessions. If the private sectors (consumers and businesses) are unwilling or unable to spend, the public sector must act as the spender of last resort.

Keynesian policy demands counter-cyclical fiscal intervention. During a recession, the government should run budget deficits, borrowing money to increase its own spending or lowering taxes to boost private consumption. This injection of demand stimulates production, puts people back to work, and leverages the multiplier to revive the economy.

"The state will have to exercise a guiding influence on the propensity to consume partly through its system of taxation, partly by fixing the rate of interest, and partly, perhaps, in other ways."

John Maynard Keynes, The General Theory (1936)

Conversely, during an economic boom when demand threatens to outstrip supply and cause inflation, the government should run budget surpluses, reducing its spending or raising taxes to cool the economy. This symmetry was essential to the theory: deficits in bad times were to be paid off by surpluses in good times, maintaining fiscal balance over the long run.

The Post-War Consensus: IS-LM and the Fine-Tuning Era

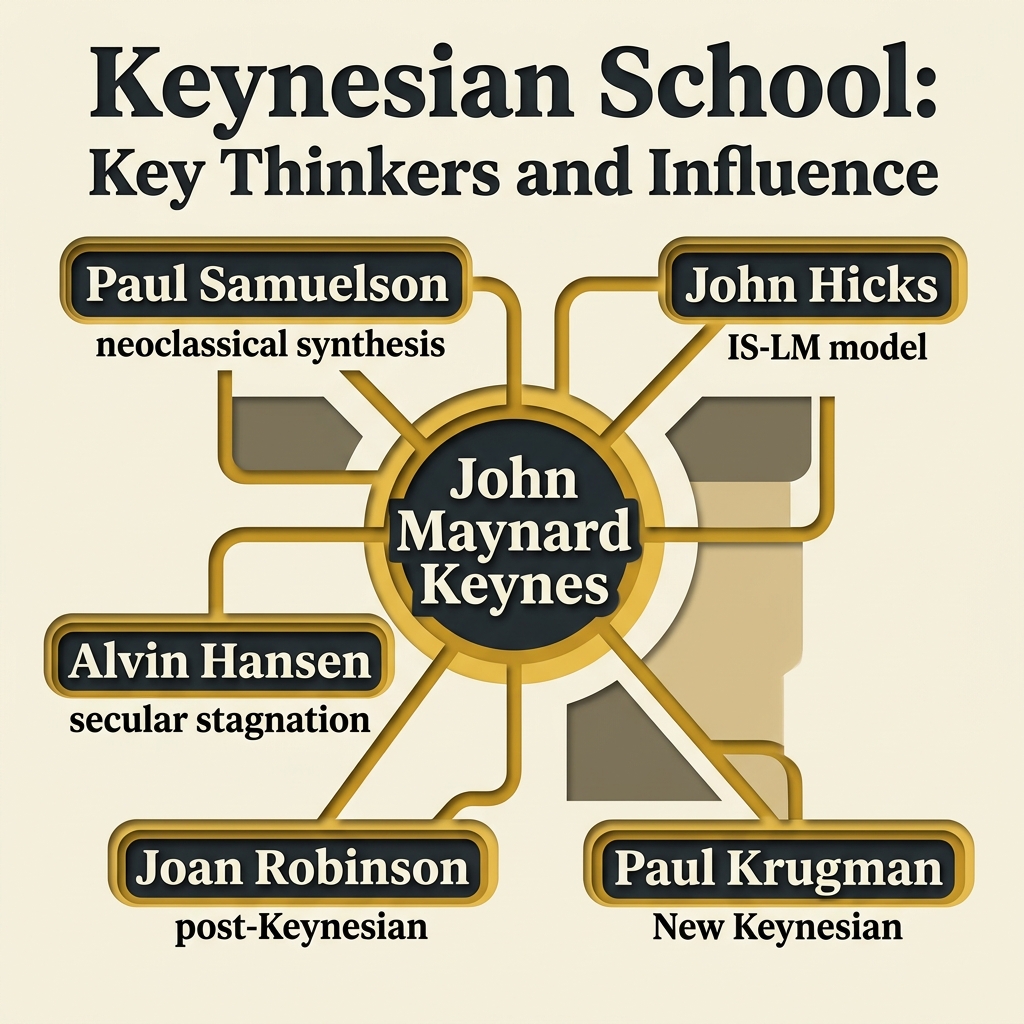

Following World War II, Keynesian ideas swept through academia and policy circles. In the United States, economists like Alvin Hansen and Paul Samuelson popularized Keynes's ideas, translating them into formal mathematical models.

The most famous of these was the IS-LM model, developed by John Hicks and modified by Alvin Hansen. The model represents the interaction of the real economy (Investment-Savings, or IS) and the monetary economy (Liquidity Preference-Money Supply, or LM) to show how fiscal and monetary policies determine total output and interest rates. This model became the standard framework for teaching macroeconomics for decades.

Another pillar of post-war Keynesianism was the Phillips Curve, named after the New Zealand economist A.W. Phillips. In 1958, Phillips published data showing a historical trade-off between inflation and unemployment: when unemployment was low, inflation tended to be high, and vice versa. Keynesian policymakers concluded they could fine-tune the economy, choosing a desired level of unemployment by accepting a certain rate of inflation.

Throughout the 1960s, this fine-tuning approach seemed highly successful. Economies grew steadily, and recessions were mild. Economists believed they had conquered the business cycle, possessing the tools to manage demand and maintain permanent prosperity.

The Crisis of the 1970s: The Failure of Stagflation

The Keynesian confidence collapsed in the 1970s. The decade was marked by a new phenomenon: stagflation, the simultaneous occurrence of high inflation and high unemployment.

According to the Keynesian Phillips Curve, stagflation was impossible. If the economy was slowing and unemployment was rising, demand was low, which meant prices should not be rising. If inflation was high, demand was high, which meant unemployment should be low. The Keynesian model had no explanation for why both were rising at the same time.

The attempt to inflate the economy out of unemployment through monetary expansion and fiscal spending only made inflation worse, while unemployment remained stubbornly high. This failure opened the door to critiques from the Monetarist School led by Milton Friedman, who argued that inflation was entirely a monetary phenomenon, and the Austrian School, which argued that government stimulus distorted the capital structure of the economy.

The Libertarian Critique of the Keynesian Model

Libertarians and free-market economists reject the Keynesian framework on both ethical and economic grounds. The primary economic criticisms can be grouped into several areas.

The Knowledge and Calculation Problem

The Austrian critique, formulated by Friedrich Hayek, is that central economic management requires knowledge that is impossible to centralize. Recessions are not simple collapses in aggregate demand; they are periods of structural adjustment. When the government spends money to stimulate demand, it does not know which sectors actually require adjustment.

Mainstream Keynesianism treats the economy as a simple machine that can be regulated by turning dials for taxes, spending, and interest rates. It aggregates millions of distinct markets, products, and choices into single variables like aggregate demand or gross domestic product. By doing so, it ignores the microeconomic reality: the price system is a delicate communication network that aligns production with consumer preferences. Government injections of spending distort these prices, sending false signals that delay the real, structural corrections the economy needs.

The Public Choice Critique: Asymmetry in Practice

Public Choice Theory, pioneered by James M. Buchanan, applies economic reasoning to political actors. It shows that Keynesian policy in practice is fundamentally asymmetric.

While Keynesian theory requires government surpluses during booms, politicians face no incentives to implement them. Raising taxes and cutting spending are politically unpopular, while running deficits and spending money on projects win votes. As a result, governments run deficits during recessions and continue running deficits during expansions. The result is a perpetual growth in public debt, the expansion of the state, and the slow debasement of the national currency.

The Distortions of Cheap Money and Debt

To stimulate demand, Keynesian policy relies on the central bank to lower interest rates and expand credit. As the Austrian Business Cycle Theory demonstrates, artificially low interest rates distort time preference signals.

Businesses borrow cheap credit to invest in long-term, capital-intensive projects that do not align with actual consumer savings and demand. This creates an artificial boom, characterized by asset bubbles (such as the housing boom of the 2000s). When the central bank eventually stops the credit expansion to prevent inflation, the boom collapses, revealing the malinvestments. Keynesian stimulus does not cure the business cycle; it creates the next bust.

Conclusion: The Persistent Legacy of Managed Demand

Despite the failures of the 1970s and the theoretical critiques of the free-market schools, Keynesianism remains the dominant operating system of modern governments. Whenever a crisis occurs, whether it is the financial crash of 2008 or the pandemic shutdowns of 2020, governments immediately resort to massive spending packages, bailouts, and central bank monetary injections.

For libertarians, the lesson of the past century is that managed demand comes at a terrible cost. It builds permanent debt burdens that drag down growth. It causes inflation that erodes the savings of the poor and middle classes. It creates a moral hazard where large corporations are bailed out at taxpayer expense, and it continuously expands the size and power of the state. Understanding how Keynesian macroeconomics operates under the hood is essential for anyone who wishes to defend a free society and a stable, voluntary economic order.