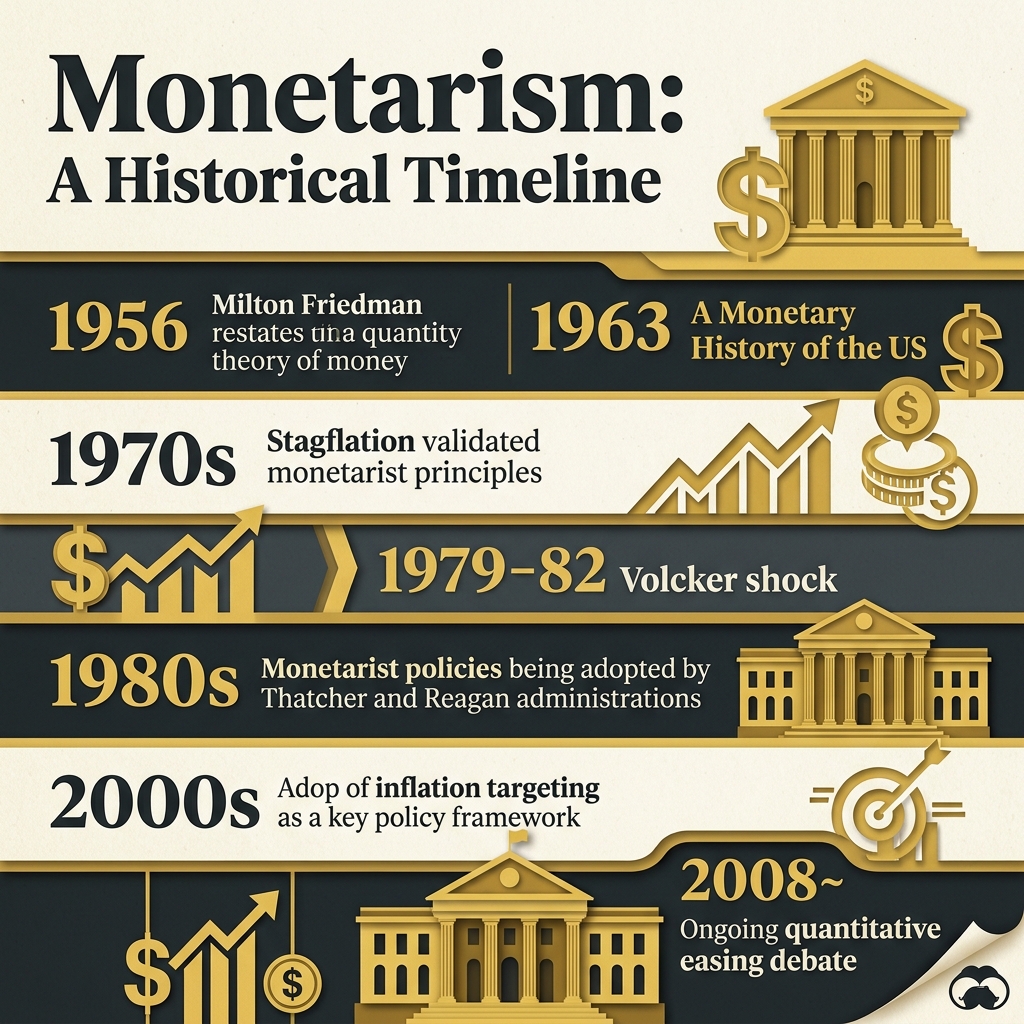

When the Keynesian consensus began to fracture under the weight of stagflation in the 1970s, the dominant counter-revolution did not come from the radical fringes of Austrian economics. It came from the University of Chicago, led by a diminutive, energetic economist named Milton Friedman. This was the Monetarist School of Economics, and for a brief, critical period, its ideas reshaped the monetary policies of the Western world.

Monetarism reasserted a classical truth that Keynesians had pushed aside: the money supply is the single most important determinant of economic activity and inflation. While Monetarism shared the libertarian preference for free markets and limited government, its willingness to preserve a state monopoly on money and a central bank to manage it drew sharp criticism from more radical free-market thinkers, particularly those of the Austrian School.

The Chicago Counter-Revolution: Resurrecting the Quantity Theory

By the mid-twentieth century, Keynesian macroeconomics had relegated money to a secondary role. Keynesians believed that monetary policy was weak, famously comparing it to pushing on a string. During a downturn, they argued, lowering interest rates would not induce businesses to invest if their expectations were low. Instead, they favored fiscal policy: direct government spending to inject demand into the economy.

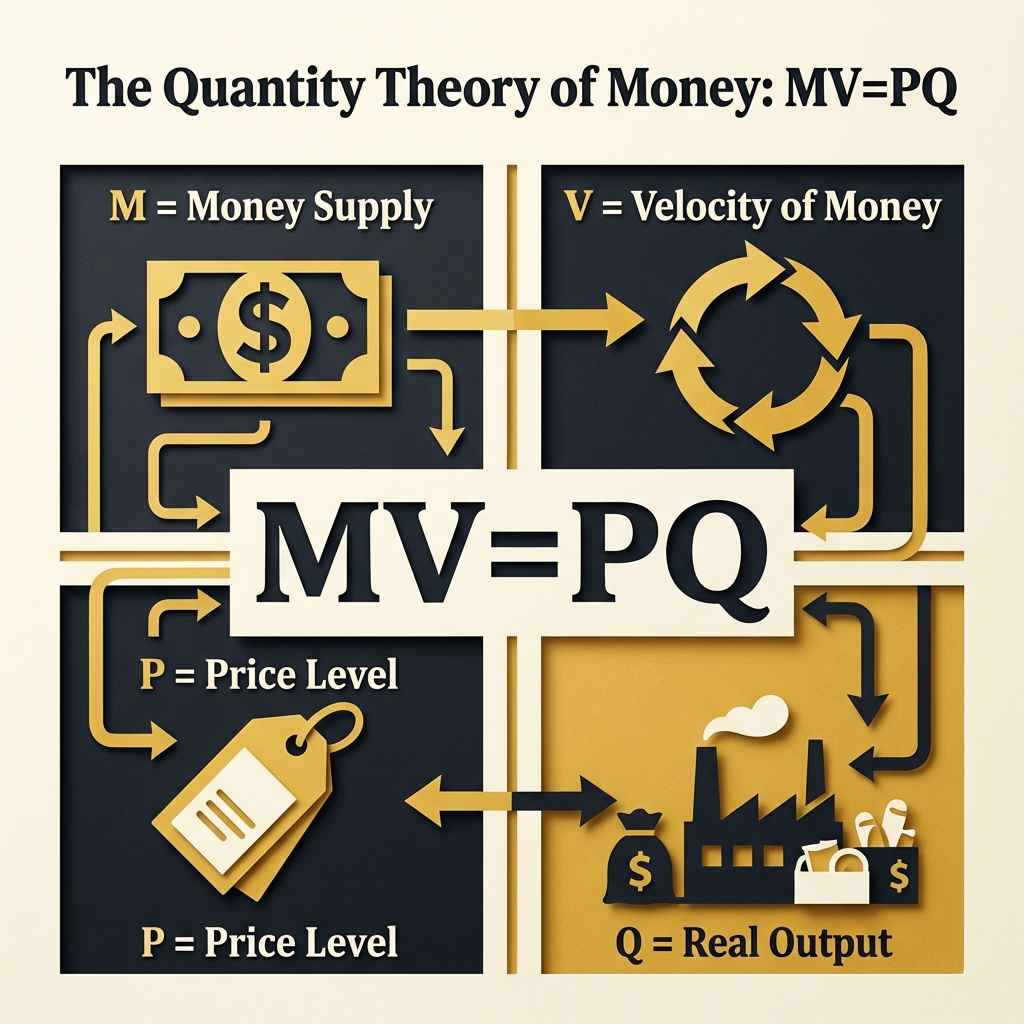

Milton Friedman (1912-2006) spent decades dismantling this view. In 1956, he published a landmark restatement of the Quantity Theory of Money. The Quantity Theory is an ancient economic concept, dating back to the Spanish Scholastics and later refined by John Locke, David Hume, and Irving Fisher. It is summarized by the equation of exchange:

$$MV = PY$$

Where $M$ is the money supply, $V$ is the velocity of money (how many times a unit of currency is spent on final goods per year), $P$ is the price level, and $Y$ is real output (GDP).

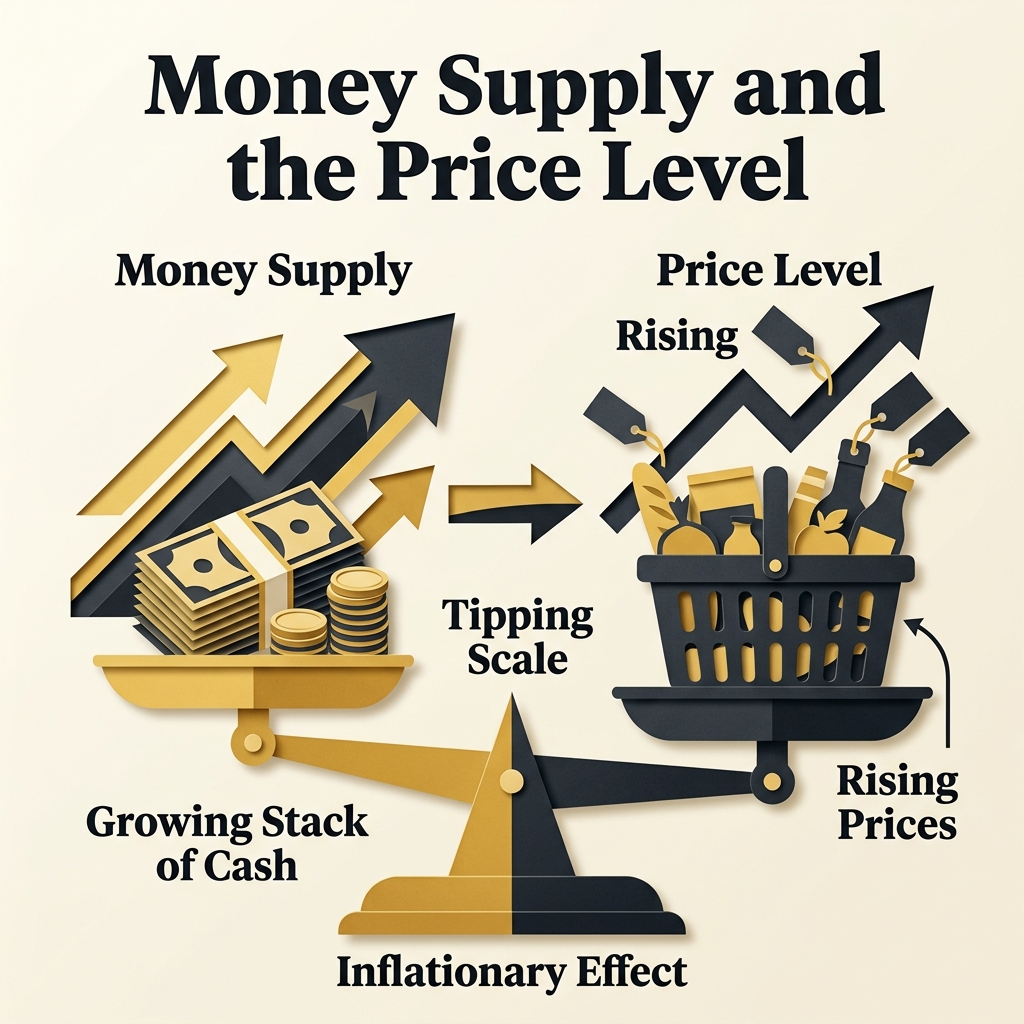

Neoclassical economists assumed $V$ and $Y$ were relatively stable in the long run. If $V$ and $Y$ are stable, then any change in the money supply $M$ must lead directly to a proportional change in the price level $P$. In other words, printing more money does not make a nation wealthier; it simply raises prices.

Friedman's contribution was to demonstrate empirically, through extensive research, that the demand for money was highly stable and that the velocity of money did not fluctuate wildly as Keynesians believed. In his monumental 1963 book, A Monetary History of the United States, 1867-1960, co-authored with Anna Schwartz, Friedman delivered a devastating blow to the Keynesian orthodoxy.

Friedman and Schwartz argued that the Great Depression was not a failure of unregulated capitalism, as Keynesians claimed, nor was it caused by a lack of investment. It was caused by a catastrophic failure of the Federal Reserve. Between 1929 and 1933, the Fed allowed the money supply to contract by nearly one-third. This contraction turned a standard economic downturn into the worst depression in American history.

Core Tenets of Monetarism

Monetarist theory is defined by several core propositions that challenged both Keynesian macroeconomics and classical assumptions.

Inflation is a Monetary Phenomenon

Friedman's most famous dictum was that inflation is always and everywhere a monetary phenomenon, in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output. Monetarists rejected Keynesian arguments that inflation could be caused by wage-push pressures from unions, cost-push pressures from oil shocks, or demand-pull pressures from a booming economy. These factors, Friedman argued, could cause temporary price adjustments in specific sectors but could not cause a sustained, economy-wide rise in prices unless the central bank validated them by printing more money.

"Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output."

Milton Friedman, Counter-Revolution in Monetary Theory (1970)

The Natural Rate of Unemployment

In the 1960s, Keynesian policy relied on the Phillips Curve, which assumed a stable trade-off between inflation and unemployment. In 1967, Friedman (and independently, Edmund Phelps) introduced the natural rate of unemployment hypothesis, which demolished this assumption.

Friedman argued that the trade-off was temporary. If the central bank attempts to reduce unemployment below its natural rate by inflating the money supply, it initially succeeds because workers and businesses are fooled by the rising prices, mistaking them for real demand growth. Over time, however, workers realize their purchasing power has fallen and demand higher wages. Employers adjust their expectations, and unemployment returns to its natural level, but with a permanently higher rate of inflation. The long-run Phillips Curve is vertical, meaning that inflation cannot buy permanently lower unemployment.

Long and Variable Lags

Monetarists argued that central banks should not attempt to fine-tune the economy through active, discretionary monetary policy. Friedman showed that the effects of changes in the money supply are subject to long and variable lags.

It takes time for the central bank to recognize an economic change, time to implement a policy response, and time for that policy to affect the wider economy (often between six months and two years). Because these lags are variable and unpredictable, discretionary policy is highly likely to be pro-cyclical. An interest rate cut meant to combat a recession might only take effect after the recovery has already begun, causing the economy to overheat and leading to inflation.

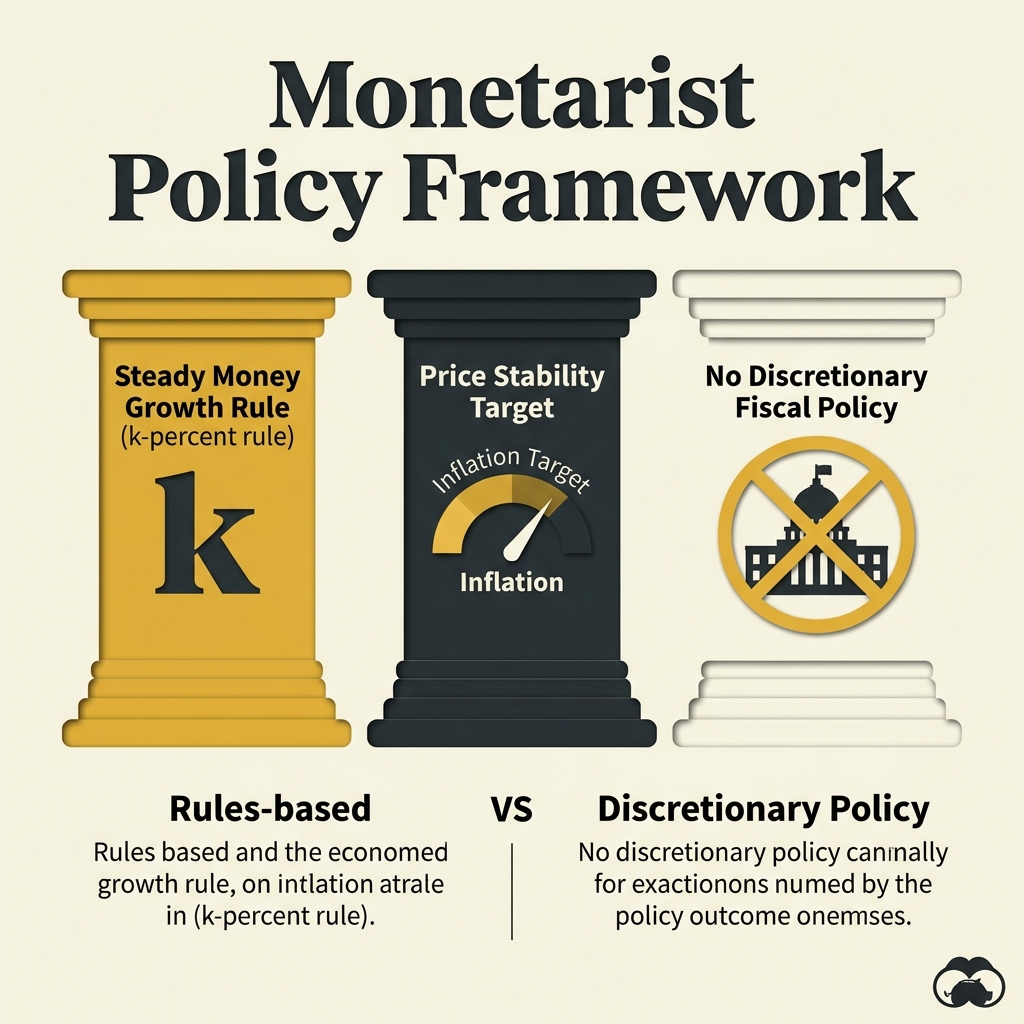

The Monetarist Prescription: The Rule-Based Economy

Because discretionary fine-tuning was dangerous, Monetarists argued that monetary policy should be governed by rules rather than the discretion of central bankers.

Friedman proposed the k-percent rule: the central bank should increase the money supply at a constant, predictable rate year after year (such as three to five percent), regardless of short-term economic fluctuations. This rate would match the long-term growth rate of real output, ensuring price stability while removing the uncertainty and political manipulation associated with discretionary policy.

Monetarism also advocated for floating exchange rates. Friedman was an early critic of the Bretton Woods system of fixed exchange rates, arguing that pegging currencies artificially distorted trade flows and forced countries to import inflation or deflation from each other. Under floating exchange rates, currency values adjust naturally to balance trade, allowing each country to pursue its own monetary policy rules.

The Libertarian and Austrian Critique of Monetarism

Although Monetarism was a free-market counter-revolution against Keynesianism, it drew sharp criticism from the more radical elements of the libertarian movement, particularly the Austrian School led by Murray Rothbard and Friedrich Hayek.

The Trap of the Monetary Monopoly

The primary libertarian criticism of Monetarism is its acceptance of a state monopoly on money. Friedman did not want to abolish the Federal Reserve; he wanted to bind it to a rule.

Austrian economists argue that this is a form of central planning. A government agency, even one operating under a rule, cannot calculate the correct quantity of money or interest rate. If the money supply is controlled by a state monopoly, it will always be subject to political pressure, and the lure of inflation to fund deficits will eventually override any rule. Hayek argued that the solution was the denationalization of money: allowing private banks to issue competing currencies, leaving the market to determine which currency was most stable.

Ignoring the Cantillon Effect

Austrian economists also criticize the Monetarist reliance on macroeconomic aggregates. The Quantity Theory equation ($MV=PY$) treats money as a neutral fluid that spreads evenly across the economy. When the money supply is increased, it is assumed that all prices rise proportionally.

In reality, newly created money does not enter the economy evenly. It is injected at specific points: through the central bank, commercial banks, and primary government contractors. The entities that receive this new money first spend it before prices have risen, capturing real resources. As the money cascades through the economy, prices rise, and those who receive the money last (wage earners, retirees) pay the higher prices with unchanged incomes. This distortion of relative prices, known as the Cantillon effect, is ignored by Monetarist models. By focusing only on the general price level ($P$), Monetarism misses the microeconomic malinvestments caused by credit expansion.

Conclusion: The Sunset of Monetarism

Monetarism reached its peak influence in the late 1970s and early 1980s. In 1979, Federal Reserve Chairman Paul Volcker implemented a Monetarist policy, targeting the growth of monetary aggregates rather than interest rates to break the back of double-digit inflation. While the policy succeeded in curbing inflation, it caused a severe recession, and the Fed soon abandoned targeting money supply in favor of targeting interest rates.

In the decades since, the relationship between money supply and inflation has become more complex due to financial deregulation and the rise of digital banking, which made defining the money supply ($M$) increasingly difficult. Discretionary policy returned, and central banks moved toward inflation targeting, using interest rates to manage demand.

For libertarians, Monetarism remains an important historical stepping stone. It proved empirically that governments are the source of inflation and that discretionary fine-tuning is a dangerous illusion. However, it also showed the limits of incremental reform. By leaving the state monopoly on money and credit intact, Monetarism left the doors open for the massive credit expansions, asset bubbles, and financial interventions that characterize the modern economic landscape.